Penfold Pension Expert Review

In this review we:

- Give our ratings based on their nearest peers

- Tell you what we think of Penfold after testing them with real money

- Highlight the key costs, facts and figures of the Penfold accounts

Penfold Expert Review: Are they a good pension provider?

Provider: Penfold Pension

Verdict: Penfold is an online provider of pensions. A digital alternative to traditional pension companies, it enables users to quickly set up a pension, and manage it online or with its app. A relatively new player in the UK pensions space, Penfold was set up in May 2018, and became regulated by the Financial Conduct Authority (FCA) in May 2019. The company was founded by three technology experts who previously worked at Deloitte and Funding Circle an since then Penfold has grown significantly since then, now serving over 100,000 users.

Is Penfold a good pension?

Yes, Penfold, was voted “Best Pension” in the 2026 Good Money Guide Investing Awards and is one of the new breed of pension providers that combines tech with personal service. Via the app, you can start a pension in less than 10 minutes and also talk to an expert advisor on the phone if you need help.

How much does it cost? Penfold is a bit pricey under £100k, but above that is very competitive. The Penfold, Standard and Sustainable plans cost 0.75% up to £100k, then 0.4% on any amount over £100k.

There is also a Sharia plan which costs 0.88% for savings up to £100k, and 0.53% on any amount over £100k.

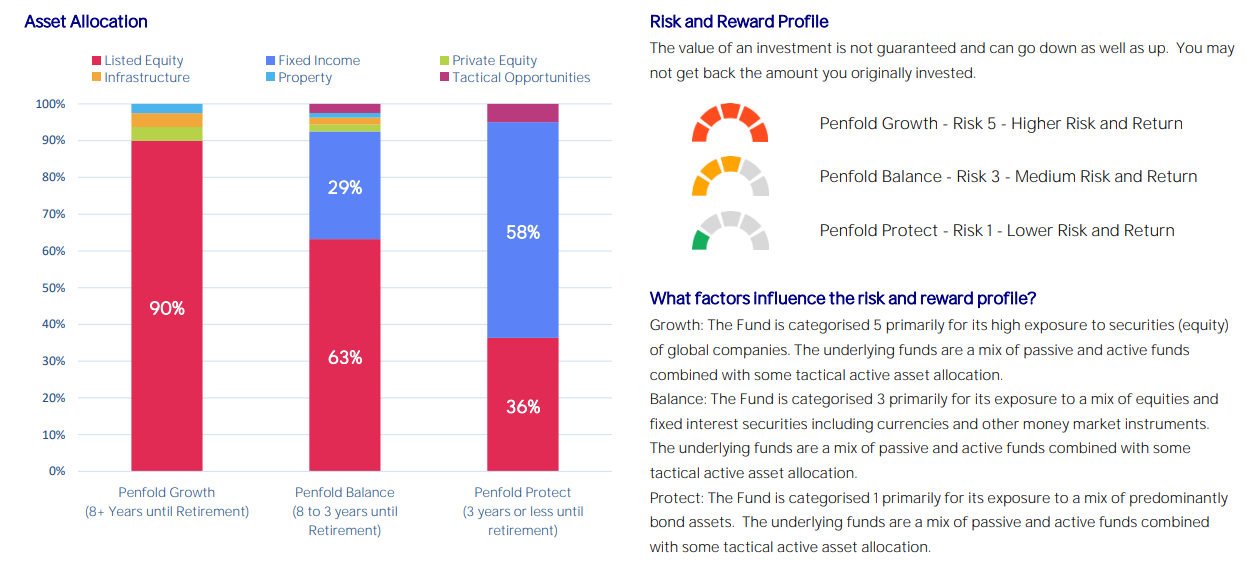

What is your pension invested in? Penfold uses Blackrock funds, which decrease in risk as you get older. So when you are young and have more time in the market, you can take on more risk, as your investments can weather the dips in the market. The closer you get to retirement, your pension will contain fewer stocks and more bonds that generate income. This means that when you actually need to withdraw your pension, it will be less likely to go down in value.

You can see in the screenshot below of the Penfold Plan what goes into your Penfold pension portfolio.

Is it easy to use? Yes, Penfold has great apps, and the website is clear. When we interviewed Christ Eastwood, the co-founder and CEO of Penfold, he told us that using technology is the key to “making pension saving easier”.

Customer Service: Penfold receives excellent customer reviews on Good Money Guide, many of which highlight great customer service.

Research & Analysis: If you are investing in this type of pension, you won’t be tinkering with it too much, so research and analysis are not that relevant. Having said that there are a lot of online resources that explain how pensions work and active social channels that aim to explain what is going on in the world of investing and pensions.

Pros

- Easy-to-use app and web interface

- Projected retirement income

- Ability to set savings goal

- Detailed insights into investments

Cons

- Relatively new company

- Slightly more expensive than robo-advisors

-

Pricing

(4)

-

Market Access

(4)

-

Online Platform

(4)

-

Customer Service

(5)

-

Research & Analysis

(3.5)

Overall

4.1

Richard is the founder of the Good Money Guide (formerly Good Broker Guide), one of the original investment comparison sites established in 2015. With a career spanning two decades as a broker, he brings extensive expertise and knowledge to the financial landscape.

Having worked as a broker at Investors Intelligence and a multi-asset derivatives broker at MF Global (Man Financial), Richard has acquired substantial experience in the industry. His career began as a private client stockbroker at Walker Crips and Phillip Securities (now King and Shaxson), following internships on the NYMEX oil trading floor in New York and London IPE in 2001 and 2000.

Richard’s contributions and expertise have been recognized by respected publications such as The Sunday Times, BusinessInsider, Yahoo Finance, BusinessNews.org.uk, Master Investor, Wealth Briefing, iNews, and The FT, among many others.

Under Richard’s leadership, the Good Money Guide has evolved into a valuable destination for comprehensive information and expert guidance, specialising in trading, investment, and currency exchange. His commitment to delivering high-quality insights has solidified the Good Money Guide’s standing as a well-respected resource for both customers and industry colleagues.