Want to build a long-term investment portfolio but don’t know where to start? Robo-advisors may be a great choice for you. These take the guesswork out of investing by matching your financial goals with pre-built portfolios of ETFs or funds. Since it’s all automated, robo-advisors are much cheaper than traditional wealth managers.

| Name | Logo | GMG Rating | Customer Reviews | Account Fees | Average Fund Fees | CTA | Tag | Feature | Expand |

|---|---|---|---|---|---|---|---|---|---|

|

|

GMG Rating |

Customer Reviews |

Account Fees 0.5% – 0% |

Average Fund Fees 0.09% |

See Offer Capital at risk |

Featured |

Features:

|

*Get up to £300 in bonus shares when you invest at least £300. Use Code WELCOME300. T&Cs apply.

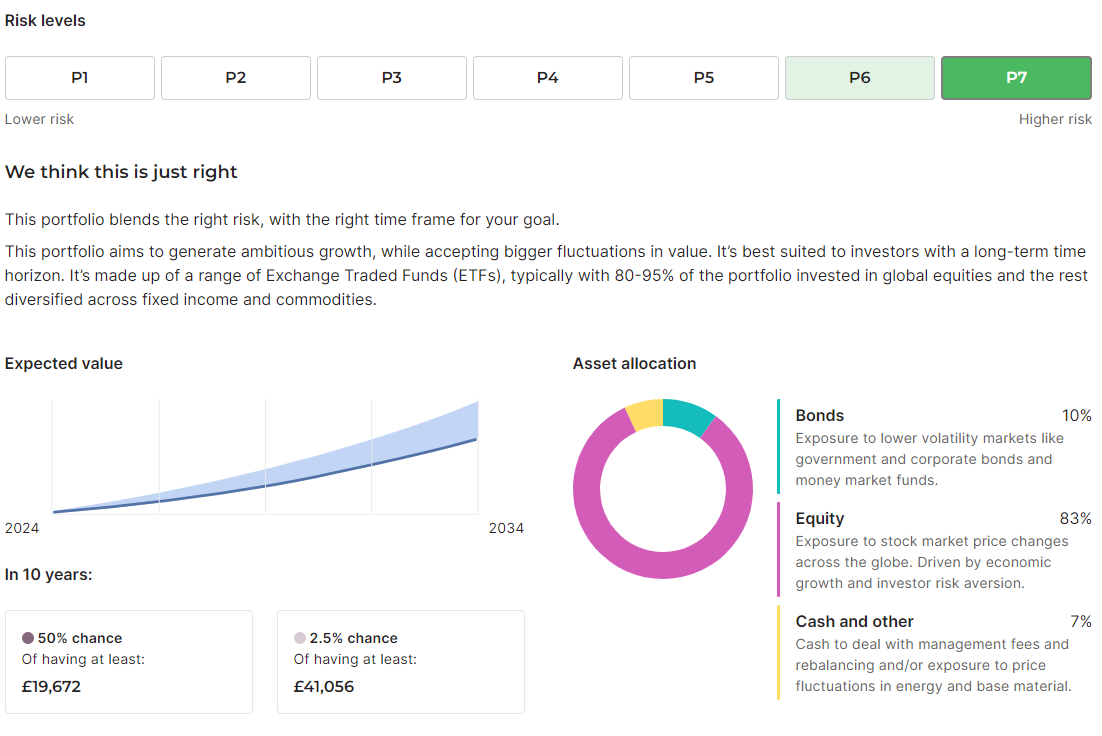

IG Smart Portfolios Expert Review: Smart Portfolios For Active Investors Are IG Smart Portfolios any good? IG Smart portfolios are a great way to invest in pre-made managed portfolios with one of the UK’s largest investing and trading platforms. IG’s robo advisor offering are cheaper than other robo-advisors, follow the well-tested Blackrock investment style in diversified portfolios. IG Group is probably best known as a provider of margin trading services be that FX, CFDs or Spread Betting, but they also acts as a stockbroker and fund manager and provide Smart Portfolios in conjunction with one of the world’s largest asset managers, Blackrock. There are six IG smart portfolios which were launched at the end of February 2017 which either replicated existing BlackRock products were created specifically for IG, by BlackRock. BlackRock is best known as an originator of ETFs and other passive investments however the products it produced for IG are not index trackers. The minimum investment for IG Smart Portfolios is £500 and you can request a withdrawal from your account at anytime and your portfolio will be reduced to cover the withdrawal amount. Fee reductions Back in 2020, IG announced that it was reducing the management fees it charges on the smart portfolios to just 0.50% per annum, and it also capped those fees at £250 a year. According to IG’s Smart portfolio price comparison, their portfolios work out significantly cheaper than robo-advisor competitors, Wealthify, Moneyfarm and Nutmeg. As IG Smart Portfolio fees are capped at £250 a year, it means that anything you invest above £50k is effectively fee-free. Investment Strategy IG Smart Portfolios are smart beta funds, rather than index trackers. Smart beta is an investment style that tries to benefit from idiosyncratic features associated with particular groups of stocks this is also known as factor investing. These factors or characteristics include traits and identifiers such as value, growth, momentum, size, low volatility and others. The thinking behind this approach is that by identifying and isolating these factors we can create portfolios which could outperform or are uncorrelated to a broad market basket. This is the type of strategy that Hedge Funds might employ. Smart beta portfolios such as those offered by IG stockbrokers aim to bring these quantitative and qualitative investment approaches to their clients, via low-cost vehicles. Performance IG Smart portfolios have a six-year track record and generally perform well. Overall the growth portfolio generated the best returns for investors, with the Aggressive fund lagging due to it’s shorter run time and early losses in 2018 doubtless caused by the sharp selloff in the markets at the end of that year. However, it’s been a bit of a rocky ride with some portfolios having losing years, especially 2022 when they all took a battering. The chart below shows each portfolio’s yearly performance but does not include 2023, which you would expect to be good seeing as the overall markets are up around 20%. Investing versus trading at IG Despite this positive performance the fund management business has not caught the imagination of the IG client base in the same way that say trading CFDs or Spread bets on equity indices have. For example, in the FY 2019 margin trading clients generated revenues of £454 million pounds for IG, whilst the investments and stockbroking division returned revenues of just £5.9 million. A positive result but a drop in the ocean when compared to the margin trading business. Since the departure of former CEO Peter Hetherington IG has made no secret of its desire to broaden both its product range and customer base. It has recently recruited both a new chairman and a head of institutional business, with that in mind. The reduction in fees, and in some cases the removal of them altogether, in the Smart portfolio’s business is doubtless aimed at growing both funds under management and annual revenues. Welcome though this cost reduction is, we can’t help but feel that the existing funds IG offers are somewhat staid when compared to what’s available elsewhere and the type of products and trading the wider group is involved in IG would surely be able to attract money to funds that replicated or in some way participated in the firm’s own trading book After all the business takes no directional view on the market but rather hedges customer flows, once the firm’s risk reaches certain predetermined levels. You can count the number of losing days that IG experiences in a year, on the fingers of one hand and surely that’s the kind return that people would be prepared to pay up for. Pros

Cons

Overall4.9 |

|

|

GMG Rating |

Customer Reviews |

Account Fees 0.6% – 0.3% |

Average Fund Fees 0.16 – 0.7% |

See Offer Capital at risk |

Features:

|

Wealthify, part of the Aviva Group, won “Best Robo-Avisor” in the 2024 Good Money Guide Awards as it lets you invest in either an original portfolio of investments from the UK and overseas or choose an ethical investment plan made from a blend of environmentally and socially responsible investments.

Wealthify Digital Wealth Management Review: Best Robo-Advisor 2025 Award Winner Provider: Wealthify Verdict: Wealthify won best “Robo-Advisor” in the 2025 Good Money Guide Awards as they offer simple, low-cost investment accounts made of pre-made diverse Original or Ethical investment plans. Owned by Aviva, customers can set their own risk/reward threshold and invest through a general investment account, stocks and shares ISA, junior ISA or pension. Wealthify Tested: Investing Isn’t A Sprint, Or Even A Marathon Anymore, It’s A Triathlon…

Investing used to be like a marathon, you’d have an annual four-hour meeting with a wealth manager who would recite your fund prices from the back of the FT, before rolling your portfolio over for his annual commission, but now it’s even harder work. To make investing interesting, robo-advisors like Wealthify (or ‘digital wealth managers’ as they prefer to be called) have been trying to democratise it and make investing open for everyone. They say, “Look, investing can be fun, if you don’t want it to be a marathon, we’ll make it a triathlon instead.” Which, as you know takes roughly about the same amount of time as a marathon, but is a swim, a bike ride and then a run. This closely translates into investing similes as, “it’s still a massive slog, but we’ll make it more interesting by giving you an app (like Strava) so you can track your performance in real-time and give you variety by risk and region”. So, by democratising investing, robo-advisors have actually made it harder. You have to make more decisions, be more involved, and you’ve now got an app so you’ll constantly be looking at (and therefore tweaking), your ISA and pension. When actually, what you should be doing is investing, then do nothing. Or should you? The Value of Compounding A while ago I interviewed the then Wealthify CEO, Andrew Russell, and one thing we discussed was how important it is to encourage people to start investing, instead of just saving. Because without the benefit of compounding returns in the long-term if you just save and don’t invest, your money will be worth less. He told me:

Clearly, if you tried to convince the young to start investing by explaining how compounding works, you’d have no customers at all. But one, thing Wealthify does really well is straight off the bat tell people how much their money “could” be worth in the future, particularly for regular investing. Which is a very powerful message to send, and one that should always be front and centre. Generally, the earlier you start investing, no matter how small, the better off you will be. When I was setting up an account, I said I would invest £1,000 initially, then £250 a month with one of their Confident plans, which Wealthify said after 25 years could be worth £122k (or £173k if the market performed better than expected). Think of the rubbish you spend £100 a month on. When I retire, I might be able to buy a Caterham, although I’ll be too old to drive it then.

It’s not entirely clear where this prediction comes from when they give it to you, but presumably, it’s based on historic returns from the various plans. Obviously, “Past performance is not indicative of future results.” If the market tanks (which it always does at some point) you’re going to be sitting on a loss. But before robo-advisors came along, if you wanted to open an account and invest with low-to-medium risk you had to go to the bank and sit down with an advisor, fill in a load of forms, and nod in bemusement as they explained why the Asia ex-Japan emerging markets fund would potentially make you more money than a treasury based fund of funds. I remember doing it, and it was exhausting, and I had just come back from working on the NYMEX oil trading floor in New York, so was in the business even back then. Thankfully now though, it’s so easy to open an account and invest, and that’s where the real democratisation of investing is. The way people are invested is basically the same, with diverse portfolios spread across asset classes and regions, albeit cheaper, with the use of low-cost funds instead of active fund managers. People have always been able to invest monthly, with even very modest amounts. But what makes investing accessible is not how it’s done, but how easy it is to get started. Even up to a few years ago, if you wanted to open an ISA account with Hargreaves Lansdown, you had to fill in a paper application and post it back. Simple Apps & Platforms Both are very easy to use with good portfolio projection tools. When setting up my Wealthify account, I didn’t even have to put in a password to get started. I managed to fund my account without getting my debit card out of my pocket, by directly linking my bank account, another massive bonus for regular investors (because if you pay by debit card and it expires, your contributions stop). I think overall it took less than five minutes to get a plan set up and funded. It’s a very slick app and website, and everything is where you expect it to be. There will always be a debate around active versus passive fund management, but the performance difference between wealth managers is generally very slim as there is a fairly standard way to create risk and region-based portfolios. Plus, if you want to beat the market, you have to take on more risk. If you just want to beat inflation, you probably won’t beat the market. Wealthify Fee Comparison One of the main advantages of robo-advisors is how cheap they are compared to traditional wealth managers (because you don’t get personal advice) and Wealthify is one of the cheapest of the bunch. Wealthify account fees are 0.6% a year of your portfolio, versus Nutmeg & Moneyfarm’s 0.75%. So if you have £100k on account, you’ll be paying Wealthify £600 as opposed to £750 for the other accounts. Over a 23-year period, that is a saving of £3,450 (and that doesn’t take into account compounding returns if you reinvested that saving). Wealthify pensions are a little cheaper, as Wealthify fees reduce to 0.3% on the portion of your pension balance over £100,000. You do, of course, have to pay fund fees on top, which are actually quite cheap with Wealthify. Wealthify say their average fund fees are 0.16% p.a. (Nutmeg & Moneyfarm are about 0.2%). Fund fees are the costs of the assets in the Wealthify plans, which are managed by investment professionals. These are higher for Ethical Plans, where the average investment costs are 0.70% p.a. Wealthify updated its minimum deposit amounts in January 2026. For the GIA, the mimimum is £1,000. Market Access You are limited to their own pre-made portfolios, but they are suitably diverse, and you can set your risk level. You can invest through a GIA, Stocks and Shares ISA or Private Pension. Unfortunately, there is no Lifetime Investment ISA to take advantage of the Government’s 25% top-up bonus. But you can invest for your children as well with a Junior Stocks and Shares ISA. Wealthify plans are made up of funds from Vanguard, L&G, HSBC, Fidelity and Mercer. All those funds charge a fee for choosing and managing the assets that the funds are invested in. If you want to know what is in the funds, you can look it up on Trustnet, see for example the HSBC America Index Fund (which is currently 28% of the Adventurous plan). So actually, just like everyone else, your investments are quite heavily linked to US tech stocks like Apple, Microsoft, Alphabet, Amazon, Tesla and Warren Buffet’s Berkshire Hathaway. Ethical Investing For the more ESG and ethically minded, you can still invest in an Ethical Adventurous plan, but assets include funds with “sustainable” in the title, like the Liontrust Sustainable Global Fund that contains stocks like 3i, a British company worth around £33bn takes a pragmatic approach to sustainable investing by influencing company boards to ensure that they assess their material environmental and social impacts and dependencies and, where relevant, support them in developing plans to mitigate ESG risks and invest in value creation opportunities that may arise. Despite that, 3i has generally performed well in recent years. Wealthify as a Business I also really like Weathify as a business. It seems there are new investing apps being set up every week, all with different USPs. But most are woefully underfunded and you have to wonder how many times they will be going back to Seedrs and Crowdcude to tap up investors because their burn rate is extortionate as they have yet to onboard a meaningful number of customers to generate revenue, or even, god forbid, make a profit. Wealthify has gone through that, but come out the other side. It was founded by Michelle Pearce-Burkestarted with £500k from Richard Theo in 2015, then a further £1m from crowdfunding on Seedrs in 2016, followed by £15m from Aviva in 2017. Even though I have invested with Wealthify, I wish I had also invested in Wealthify, but that’s a whole other story and one with a completely different risk appetite. Aviva Backed for More Security Being Aviva owned is great for clients because it offers a huge amount of financial security, and of all the robo-advisors out there only Wealthify and Nutmeg (JP Morgan), have the backing to ensure that they may still exist in twenty years time. This is important because investing isn’t like using a credit card or buying car insurance, where you can switch every year. When you invest, you may well be with that provider for 50 years. When I interviewed Linsey Rix, the head of UK Savings and Retirement at Aviva, one of the reasons they were so interested in Wealthify was it gives them a chance to get people investing, who may have been put off by the established and grown-up nature of Aviva. She told me:

You can tell Wealthify is owned by one of the bigger boys like Aviva as well, because even though it is very easy to set up an account, they are still heavy on the compliance. I actually failed the suitability test. I filled it in as though I was a beginner investor and was told I couldn’t invest because I didn’t understand the risks of stock market investing. Although, I re-took it with a greater appreciation for risk and was granted permission to create a plan. But it’s a good example, of how whilst everyone should be able to invest, not everyone should actually invest. After all, just like training for a triathlon, if you do it with friends it is easier, and just like investing if you take an active interest in your health you will be healthier and wealthier in the long run. Customer Service Wealthify is rated highly for support from real people in Wales, so you can handle most issues online, but also have the ability to phone straight through for more complex issues. Research & Analysis Some good analysis around portfolio rebalancing, although it’s mainly passive commenatry updating on performance rather then ideas on what to invest in. But this is not surprising as Wealthify is very much a “invest and forget platform”. So much so that When I tested the platform and set up some regular investments, I am genuinely surprised when I log on and see them. The way a long term investing account should be. Pros

Cons

Overall5 |

||

|

GMG Rating |

Customer Reviews |

Account Fees 0.75% – 0.35% |

Average Fund Fees 0.1% – 0.21% |

See Offer Capital at risk |

Features:

|

Moneyfarm Digital Wealth Management ReviewProvider: Moneyfarm Verdict: Moneyfarm is a digital wealth manager that aims to make personal investing simple and accessible. It was launched initially in Italy in 2012 by Italian bankers Paolo Galvani and Giovanni Dapra and entered the UK in 2016 and has big-name financial backers such as Allianz Global Investors, Cabot Square Capital, United Ventures and Poste Italiane. Is Moneyfarm any good for wealth management? Yes, Moneyfarm is more of a digital wealth manager rather than a robo-advisor as the portfolios are put together by investment managers, rather than automatically. The automation, as it were, is fine-tuning your portfolio to match your risk/reward choices. Unlike with other robo-advisors, with Moneyfarm you can also top up your portfolio with individual shares and ETFs. Fees: Moneyfarm charges 0.75% to 0.6% up to £100k then 0.45% to 0.35% over £100k. Moneyfarm investing account fees are scaled between 0.75% for accounts between £500 and £50,000, then above £100k are 0.45% to 0.35%. Average investment fund fees are 0.2% and the average market spread when buying and selling is 0.10%. Market Access: You can invest in 7 pre-made portfolios, but also (unlike a lot of other digital wealth managers and robo-adviors) also buy individual shares, ETFs, bonds and mutual funds online. It’s a bit of a shame you can’t buy US stocks, But Moneyfarm is best really for setting up regular investments in a GIA, ISA or SIPP, then letting them grow over time without too much tinkering and speculating on Tech stocks. App & Platform: It’s really easy to use, plus it puts you through your paces to make sure you understand what you are investing in. Apparently, my Moneyfarm investor profile is “pioneering”, which means I want to take on more risk for potentially better returns. Customer Service: This is mostly online as you’d expect but solves all issues – I’ve had some good calls with Moneyfarm about how its products work over the years, and its people really know their stuff. If you want to find out more about the ethos, you can read my interview with the CEO Giovanni Daprà on how they are so much more than a robo-advisor. Research & Analysis: Not much to speak of other than a few guides, but that’s ok, as I don’t really want Moneyfarm spamming me with stock trading ideas.

Pros

Cons

Overall5 |

For years people have been trying to make investing interesting, but it’s not, it’s dull. Trading is fun, high-risk, fast, dangerous and like sprinting. But, like trying to run too fast, especially when you hit 40, you’ll probably injure yourself just as in trading, you’ll probably lose money.

For years people have been trying to make investing interesting, but it’s not, it’s dull. Trading is fun, high-risk, fast, dangerous and like sprinting. But, like trying to run too fast, especially when you hit 40, you’ll probably injure yourself just as in trading, you’ll probably lose money.

We Only Recommend FCA-Regulated Robo Advisors

We Only Recommend FCA-Regulated Robo Advisors

All robo-advisors that operate in the UK must be regulated by the FCA. The FCA is the Financial Conduct Authority. They ensure UK digital wealth managers are properly capitalised, treat customers fairly and have sufficient compliance systems.

Not only are our top picks FCA-regulated, but you’re also protected by the FSCS (Financial Services Compensation Scheme).