Use our stocks and shares ISA calculator to see how much tax free profits you can generate by investing instead of saving.

How To Use Our Stocks & Shares ISA Calculator

Here’s a step-by-step guide on how to use the Good Money Guide Stocks & Shares ISA Calculator and what to watch for. This calculator helps you see how much a Stocks & Shares ISA (for adults) might grow over time, based on how much you put in, how long you invest, and what rate of return you assume. It shows:

- Final ISA Value: your projected pot size

- ISA Contributions: how much you’ve put in

- ISA Returns: how much of that final value is growth (profit)

It’s useful for comparing different savings rates, time horizons, or return assumptions.

| Field | What it means | Tips |

| Initial ISA Contribution | A one-off lump sum you invest right away | If you’re starting from zero, use 0 |

| Expected Annual Returns | The rate you expect your investments to grow | Default is 5 %. You could test lower (e.g. 3 %) or higher (e.g. 7 %) |

| Monthly ISA Contribution | How much you’ll add every month | This is in addition to the initial amount |

| Years Invested | How many years you plan to leave the money invested | E.g. if you plan to invest for 10 years, enter 10 Good Money Guide |

Once you put in those inputs, the calculator gives you:

- Final ISA Value

- Total Contributions

- ISA Returns (i.e. “growth above your contributions”)

How to calculate your Stocks & Shares ISA returns

- Go to the Stocks & Shares ISA Calculator page.

- Enter or adjust the Initial ISA Contribution.

- Set your Expected Annual Return (e.g. 5 %).

- Put in the Monthly ISA Contribution you plan to make.

- Enter Years Invested (how long you’ll leave the money invested).

- Click “Calculate” (or the equivalent).

- View the outputs: Final Value, Contributions, Returns.

Try changing the inputs (e.g. increasing monthly contribution, changing return assumption, lengthening years) to see how much difference those make.

Key Things to Remember & Caveats

- The calculator does not include fees, platform costs, fund management fees, trading fees are not factored in.

- The rate of return is an assumption, not a guarantee — market performance can be wildly different.

- Contributions are limited by the annual ISA allowance (for stocks & shares ISAs).

- Growth and withdrawals within an ISA are tax-free, which is a key advantage.

- If you withdraw, you may lose the tax-efficient “wrapper” on that money (if the provider doesn’t allow replacing it).

How the Stocks & Shares Calculator Works

Let’s run a sample:

- Initial ISA Contribution: £1,000

- Monthly Contribution: £200

- Expected Annual Return: 5 %

- Years Invested: 15

You’d enter those into the calculator. It might output something like:

- Total Contributions: £1,000 + (15 × 12 × £200) = £1,000 + £36,000 = £37,000

- Final ISA Value: ~ £48,000–£55,000 (depending on compounding)

- ISA Returns (Growth): ~ £11,000–£18,000

So your contributions of £37,000 over 15 years might grow to £50,000+ under that 5 % assumption — entirely tax-free inside the ISA.

Ready to start investing in a stocks and shares ISA?

| Name | Logo | GMG Rating | Customer Reviews | ISA Annual Fees | Dealing Commission | CTA | Tag | Feature | Expand |

|---|---|---|---|---|---|---|---|---|---|

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0.3% |

Dealing Commission £10 |

See Offer Capital at risk |

Award Winner 🏆 |

Features:

|

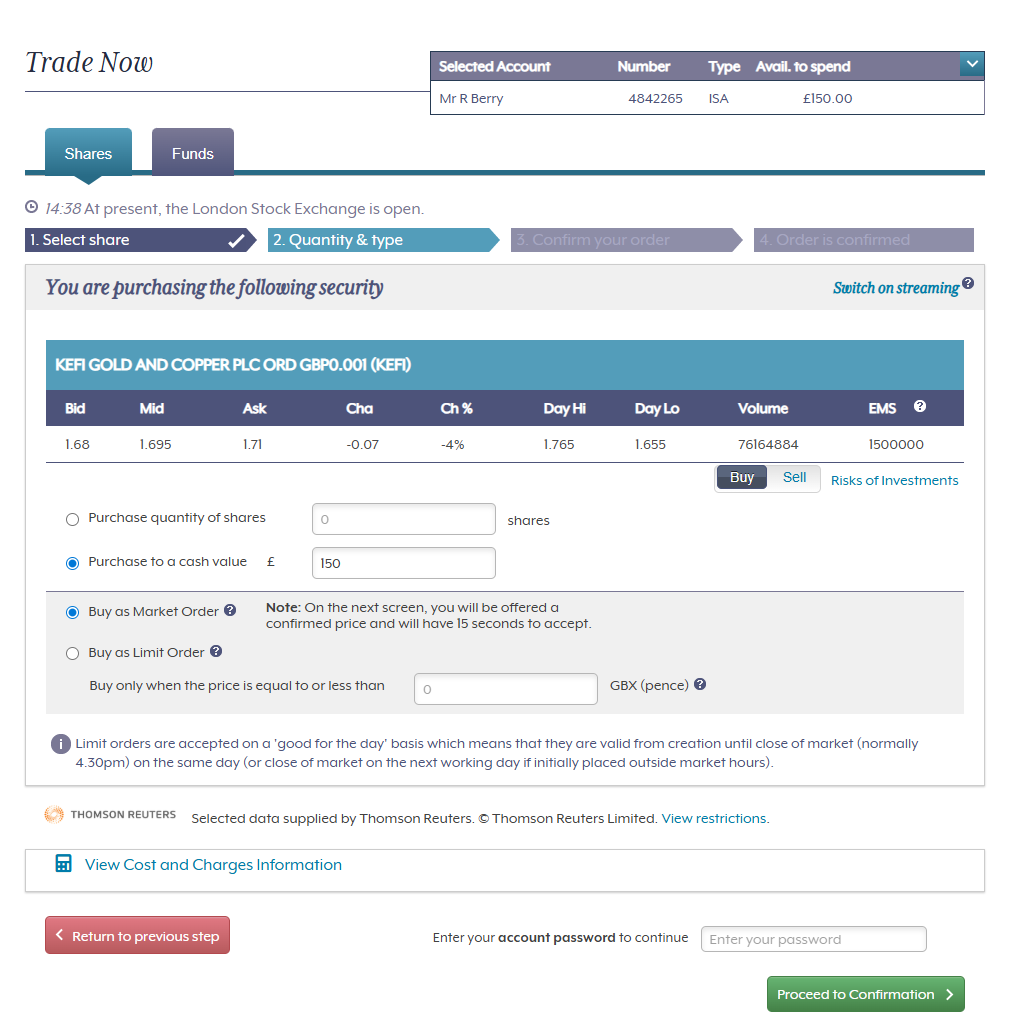

Charles Stanley Direct Stocks & Shares ISA Review: Voted "Best Stocks & Shares ISA" in the 2026 Good Money Guide Investing Awards Account: Charles Stanley Direct Stocks & Shares ISA Description: Charles Stanley Direct's Stocks & Shares ISA was voted "best stocks and shares ISA" in the 2026 Good Money Guide Investing Awards. It's a good choice for longer-term UK investors with larger portfolios (as fees are capped across all account types) and for those that value customer service above tech. Is Charles Stanley Direct's Stocks & Shares ISA any good? Yes, we rate Charles Stanley Direct’s Stocks & Shares ISA very highly, especially for investors with larger portfolios and those that want added value and excellent customer serivce. Pricing: Charles Stanley Direct charge 0.3% of the value of your investments, but fees are capped across all accounts at £600, and there is a minimum ISA fee of £60. There is also a £10 online share dealing fee, so it’s certainly not the cheapest ISA around and best suited to those with larger portfolios. FX is a little punchy too. If you are buying US stocks, 1% below £10k and 0.75% up to £50k is quite high compared to peers. Above £50k, 0.5%, which is a bit more reasonable. However, as with everything in life, you get what you pay for. If you want better service and access, it will cost a little more. Market Access: Excellent – one of the great things about old school stock brokers is that you can invest in all the weird and wonderful small-cap stocks on the London Stock Exchange. For some reason, Kefi is one of the most popular share price pages on Good Money Guide at the moment, even though it is only a tiddler valued at £180m, people seem to be really interested in it. That is, despite the investor relations page being described by one of our analysts as “like something from the bad old days of bulletin boards”. But, opinion, as they say, is what makes a market, so I bought some Kefi shares as a test trade when I was testing their ISA. After all, when we interviewed Charles Stanley Direct’s Chief Analyst, Rob Morgan after they were voted best ISA, he said there was a lot of value to be had in the small-cap market, which I happen to agree with, so I can’t blame him if they go down. App & Platform: I’ll be honest, the desktop version could do with a refresh; it’s a bit 2006, but does the job. The app is much slicker. I was surprised to hear that only around 25% of orders go through the app at the moment. There is much more stock info on the app, like what the company does, performance and some dividend info. It’d be good to get some analyst ratings and broker forecasts on there, plus a recurring order function would be handy (good investing habits and all that). But you can choose to invest on an amount basis, rather than per share basis, which is the modern way.

Customer Service: This is where stock brokers differ from investment platforms, and I think where Charles Stanley Direct is winning. Investors get to a point where their portfolio has grown to a level where it’s quite nice to have a chat with someone about it. One of the recurring themes of the reviews that are left on Good Money Guide for Charles Stanley Direct is that the customer service is excellent, and the ability to get advice or guidance from a broker is one of the key draws to traditional stock brokers as opposed to online or app-only platforms. Research & Analysis: There is lots of on-trend analysis available to read from experienced analysts, a good knowledge base to find out more about ISAs and SIPPs. But I think the main thing here in the AI world we currently live in is the ability to pick up the phone and have a chat. Pros

Cons

Overall4.6 |

|

|

|

GMG Rating |

Customer Reviews |

ISA Annual Fees £59.88 |

Dealing Commission £3.99 |

See Offer Capital at risk |

Features:

|

Interactive Investor Stocks & Shares ISA Combines DIY & Managed PortfoliosAccount: Interactive Investor Stocks & Shares ISA Description: Interactive Investor has previously won the Good Money Guide award for best stocks and shares ISA account as they offer one of the cheapest investment ISAs that provides access to over 40,000 shares and 3,000 funds, as well as investment trusts, ETFs and bonds. They are a good choice for people that want to take control of what they invest in. Is the Interactive Investor ISA any good? Yes, we rate the Interactive Investor ISA as very good, especially for high-value accounts as the account costs do not rise with your portfolio value. Plus, there are DIY and managed ISA options. However, for smaller accounts, the fixed monthly fee is expensive, so ii is a better ISA account for larger investors. Special Offer: Between 1 September and 31 October, new customers opening an ISA , as well as existing customers adding an ISA, can benefit from £50 worth of free trades. There is no minimum deposit required to qualify. When the interactive investor managed stocks and shares ISA turned 1 year old, we open an account, to test the platform, performance and compare it to other providers. II does not charge any additional fees for a Stocks and Shares ISA, over and above its standard trading account charges. Whilst competitors Hargreaves Landsdown and AJ Bell both charge annual custody fees based on the value of your holdings. How does the managed ii ISA work? interactive investor offers both a self-managed stocks and shares ISA and a managed option, which means that you can either make your own investment decisions or buy into a pre-made portfolio. One of the key advantages about the ii ISA is that you can invest in smaller-cap shares on the AIM market which you cannot do with other investment apps like Lightyear or Freetrade. The Managed ISA is designed for investors who want to hold investments in a tax-efficient ISA wrapper, but who don’t have the time, or inclination, to research and select investments themselves. These are similar to what robo-advisors offer like Nutmeg, Wealthify and Moneyfarm, Low-cost trackers or sustainable investing There are two options: lost-cost index trackers, and a sustainable plan, but that is more expensive with investment costs (charged by investment manager, not ii) of 0.25%-0.29% versus 0.13% – 0.2% for the non-sustainable option. However, with the sustainable portfolio only 55%-90% of your investment is in sustainable funds (depending on how much risk you take). But how sustainable are they? For instance, the biggest allocation of the sustainable portfolio is 33% in the iShares US ESG Index Fund, if you take on the most risk, which mainly consists of big US tech stocks like Apple (6.76%), Microsoft (5.81%) and Nvidia (3.21%). This is opposed to the standard index tracker where the two largest holdings are abrdn American Equity Tracker (16%) which is 6.5% Apple stock and the L&G US Index Trust which has 6.45% Apple stock. So you’re really only investing a small about in sustainable investments and being charged a lot more for it. Performance When I opened an II managed ISA to test them out I went with the minimum £250 initial deposit and set up recurring monthly investments of £50 in the Level-5 very adventurous portfolio, which according to ii would net me healthy £8,030 if the market performed as expected from £6,250 contributions (a profit of £1,780) which they calculate on assumed returns of 5%, which is a bit dull in my opinion, especially when the fees are going to be £144.55 a year or £1,445.50 over 10 years, essentialy halving my returns. more on that later. These portfolios have just turned a year old so I wanted to have a quick look at how well they had done, but alas, ii does not publish this info. When I phoned customer services (got straight through) to find out more they said they don’t have the info but woudl let me know when they do and I will let you know to. Which I thought was odd becuause the entire reason I updated this ii managed ISA review was becuase I just received an email titled “Managed ISA turns 1 — ready to join the club?” No I know that past performance is no reflection of future returns, (the risk warning that must apply to all investing) but I’d at least like to see a chart that can tell me if it has made or lost money in the past. Not just a bog-standard estimation based on assumed returns. I hope this gets better in the future, as clearly no-one is going to want to invest in a poorly performing product, and not being able to see historic returns sort of implies there is something to hide. Even if there isn’t.

How does the II-managed ISA compare to the competition? interactive investor’s flat monthly fee charging structure will save ISA investors money over the long term. Which brings me back to my point about ii being expensive for small portfolios. But, if you invested all £20,000 of your ISA allowance with ii, your estimated profit on the same basis would be £11,900 with £1694.80 in fees over ten years, which is less than 15% of your returns Compare this to other managed ISAs like Wealthify who charge 0.6% where if you added your full allocation to your ISA each year your fees would be around £8k, but as interacitve investor fees are fixed, you would save nearly £6k. According to calculations on their website, £50,000 held in an ISA with the platform for 30 years, would have grown to almost £1.20 million, assuming a growth rate of 5.0% per annum, in a mixed portfolio of funds and shares. That’s up to £45,000 more than you would have returned at rivals like Hargreaves Lansdown, AJ Bell, Fidelity, and Barclays Smart Investor, according to the Interactive Investor data. In terms of ISA fees Hargreaves Lansdown offers a a tiered fee structure based on the value and type of investments held. Those fees start at 0.45% for sums up to £250,000 invested in funds, falling to 0.1% between £1.0 and £2.0 million, with no charges levied for investment amounts over £2.0 million. There are no additional fund dealing charges. Money that’s invested in UK and international shares and ETFs, in a Hargreaves Lansdown ISA, attracts a maximum monthly fee of £3.75 and trading charges start at £11.95 per deal, with volume discounts down to £5.95 applied one month in arrears. AJ Bell levies a fee of 0.25% of the first £250,000 invested. However, that scales down to zero if you have more than £500,000 in your account. Share deals, including ETFs, are charged at £5.00 per trade, which falls to £3.50 if you traded 10 times or more in the prior month. Whilst fund trades cost £1.50 a pop. Pros

Cons

Overall4.8 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0.6% |

Dealing Commission £0 |

See Offer Capital at risk |

Features:

|

Wealthify Stocks & Shares ISA Is Great For Pre-Built Portfolios Account: Wealthify Stocks & Shares ISA Description: Wealthify has an excellent stocks and shares ISA and won Best Robo Advisor at the Good Money Guide Awards 2024 and 2025 due to its high scores in our consumer survey, exceptional customer service, broad market access, and diverse portfolio offerings, as well as excellent reviews from users. It's a good choice for beginner investors who want an easy-to-use, cost-effective investment ISA that offers access to products that are well suited to new investors, such as ready-made portfolios, where you can get started with as little as £1,000 to invest. Capital at risk. The Test: Is Wealthify's Investment ISA Good? Yes, I’ve tried it out and I think Wealthify has a good stocks and shares ISA, which is why I opened one when my wife and I decided not to replace our cleaner when she left to return to Brazil. This departure meant we had an extra £65 a month in the Berry coffers. But what to do with the money? Mrs Berry said she would put it in her Lloyds account. I said this was a terrible idea as Lloyds was paying her a pitiful 1.1% interest – less than inflation and far less than the Bank of England interest rate of 3.75%. In real terms, we’d be losing about £12 a year. There’s a Wealthify Cash ISA for if you don’t want to take any risk, but as we were happy to put the money away for the long term, we plumped for an investing ISA. One of the things I’ve always liked about Wealthify is that it tells you how much money you could make in the future. One of the simple steps the app takes you through when setting up your ISA is to let you play with a slider that gives you a projected future value of your portfolio based on how much you regularly invest and how much risk you’re willing to take. The app also very easily shows you what you are invested in and your returns so far. The Portfolio I Picked As I considered the £65 per month to be semi-found money, and I’m a natural risk taker, I opted for the highest risk portfolio with the best potential returns. Typically, I failed the suitability test (a questionnaire that’s pointless for experienced investors, but has its uses if you’re a beginner) as it told me that I didn’t understand the risks I wanted to take and should go for a lower risk portfolio. But if I’d taken less risk, my projected returns over 10 years on a £65 initial investment, with contributions of £65 a month, would have been £9,761.39 instead of £10,526.43, which is a difference in potential profit of over 40%. So I took the test again, changed a few bits, passed and opted for the higher risk portfolios, which contain 77.74% shares. If I’d opted for the lowest risk portfolio, I would have been buying 76.92% bonds. These are income-generating investments that generally rise in value less than shares do, but are considered safer. I wanted to see exactly what I was investing in, so I viewed the Wealthify Adventurous Plan Factsheet which gives the full portfolio breakdown; the kicker is the 28% allocation to the HSBC America Index fund which contains the usual Apple, Microsoft, NVIDIA, Meta and Alphabet tech stocks that have held up international markets over the last few years. I must say at this point that past performance is no indication of future returns. Because, as we well know, the stock market can crash at any time. 👀 Having said that, crashes are, in my opinion, usually a good time to invest because the market generally rises again, and the major indices contain the biggest and most profitable public companies. If those companies start to lose money, they are replaced by others that are are doing better, and so on. Overall, my Wealthify investment ISA was up and running in about 4 minutes, which was less than the time it took to drink my morning cup of coffee whilst my wife explained that it would now be my responsibility to do the vacuuming on Saturdays. I should note that since I opened my Wealthify ISA the minimum initial deposit is now £1,000, presumabley because Wealthify doesn’t make any money from small accounts. Or maybe they want to encourage people to invest more… Market Access Wealthify’s Stocks & Shares ISA offers 5 investment options: Cautious, Tentative, Confident, Ambitious, and Adventurous. All of these strategies have a mix of low-cost passive and active funds. Funds contain a collection of investments and are a convenient and cost-effective way to invest. Investors also have the option to build an ethical portfolio. One downside to Wealthify is that, there are only a few investment options to choose from and not much flexibility – you can’t invest in individual shares and funds. Fees Wealthify charges an annual fee of 0.60% for managing your investments. This means it’s not quite as cheap as InvestEngine (0.25%) which has some ETF portfolios, but it’s cheaper than Moneyfarm (0.75%) where you can invest in individual shares and bonds. The other costs of the Wealthify ISA to consider are the Wealthify Investment Plans’ fund and trading fees, which are charged at 0.15% by the fund managers to run the funds that Wealthify invests in. Investment fees are fairly non-negotiable and are standard for all investment platforms. However, some robo-advisors or digital wealth managers choose different products with different costs. For example, the underlying fund fees Moneyfarm charges are 0.2%. Wealthify’s Ethical Portfolio There is an ethical investment portfolio available on Wealthify, where fund costs are 0.58%, but performance has typically been worse, and I personally think the ESG investing thing is a load of greenwashing. For instance, the 2 biggest funds in the Wealthify Ethical Portfolio are the Brown Advisory US Sustainable Growth Fund (22%) and FTGF ClearBridge US Equity Sustainability Leaders Fund (16%), which both have as their top 3 holdings… Microsoft, Amazon and NVIDIA. But to be fair, its third largest fund is the Liontrust Sustainable Future UK Growth Fund. In this fund, the biggest holding is 3i, whose biggest portfolio investment is Action, a Dutch non-food retailer with double decker trucks that are said to carry 60% more than a regular truck, which is apparently “better for the environment and better for your wallet”. Wealthify’s Stocks and Shares ISA vs Cash ISA With a Wealthify investment ISA, your money is in a mix of funds and that mix depends on your attitude to risk. A Wealthify investment ISA is a good choice if you’re investing for more than 5 years. But if you want no risk, and you’re putting money into an ISA for the short term, a Wealthify Cash ISA may be more appropriate. Both these ISAs are flexible, meaning you can withdraw and replace funds during the same tax year without impacting your annual ISA allowance. You have to replace funds into the same ISA you withdrew them from. Pros

Cons

Overall4.7 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0% - 0.75% |

Dealing Commission £3.95 |

See Offer Capital at risk |

Features:

|

Moneyfarm Stocks & Shares ISA Review: A digital wealth manager that lets you buy individual sharesAccount: Moneyfarm Stocks & Shares ISA Description: Moneyfarm’s ISA invests in ETFs to keep the costs low, so you aren’t paying for active managers. Instead, you are benefiting from tracking a series of diversified indices that are regularly rebalanced. This should mean you get to keep most of your returns rather than paying hefty fees to fund managers.

Is the Moneyfarm ISA any good? Moneyfarm has a stocks and shares ISA that invests your money in the stock market. You can get better returns than with a cash ISA, but as with all investing the stock market goes up and down so you could get less than you originally invested. So if you don’t want to risk losing any money a cash ISA with someone like Hargreaves Lansdown Active Savings would be a better option. Fees: Moneyfarm’s ISA investing account fees are scaled between 0.75% for accounts between £500 and £50,000, then above £100k are 0.45% to 0.35%. Average investment fund fees are 0.2% and the average market spread when buying and selling is 0.10% Pros

Cons

Overall4.9 |

||

|

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0% - 0.25% |

Dealing Commission £3.50 - £5 |

See Offer Capital at risk |

Features:

|

AJ Bell Stocks & Shares ISA Review: Excellent all-round low-cost ISA investingHow does AJ Bell's ISA work? AJ Bell’s ISA is a stocks and shares ISA which means that you are invested in the stock market. AJ Bell does not offer cash ISA like Hargreaves Lansdown do with their Active Savings product. However, AJ Bell do pay interest on uninvested cash so if you want to keep some money outside the risks of the stock market you can earn interest on your cash. Fees: AJ Bell charges 0.25% of the value of your portfolio for their ISA. But, share account fees are capped at £3.50 a month. Dealing costs are £1.50 for funds and £5 for shares but drop to £3.50 where there were 10 or more online share deals in the previous month. AJ Bell Special Offers:

Pros

Cons

Overall5 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0% - 0.45% |

Dealing Commission £5.95 - £11.95 |

See Offer Capital at risk |

Features:

|

Hargreaves Lansdown Stocks & Shares ISA Review: Compounding is the key to successAccount: Hargreaves Lansdown Stocks & Shares ISA Description: Hargreaves Lansdown’s Stocks & Shares ISA offers access to a vast range of investments. Investors have access to domestic and international equities, over 4,000 funds, bonds, and more. Another advantage is that the platform offers plenty of research and investment tools to help you make investment decisions. Is Hargreaves Lansdown's Investment ISA: Is it any good? Yes, we consistently rate Hargreaves Lansdown’s stocks and shares ISA as one of the best in the industry, particularly if you are investing in individual shares. You can also invest in a cash ISA through their Hargreaves Lansdown Active Savings account. Hargreaves Lansdown was ranked as the best self-select investment ISA in 2023 in our awards, as they offer a huge range of investment options backed up by industry-leading customer support and research. Popularity: Hargreaves Lansdown’s Investment ISA is incredibly popular with over 955,000 stocks and shares ISA currently active. Fun fact: An HL ISA is gets opened or topped up via the website or app every 6 seconds during the busiest hour on the last day of the tax year (between 3pm-4pm). Special Offer: As it’s ISA season, until 5 April 2025, Hargreaves Lansdown (HL) is offering any new or existing clients transferring or contributing a minimum of £10,000 into a newly opened HL Stocks & Shares ISA and/or SIPP cash back between £100 and £3,000. Clients transferring into an existing HL Stocks & Shares ISA / HL SIPPs are also eligible. In addition, clients topping up their HL Stocks & Shares ISA, Lifetime ISA, Cash ISA or SIPP by a minimum of £3,500 in one single product, will be automatically entered into a prize draw for two chances to win £50,000. Fees: Hargreaves Lansdown’s ISA costs 0.45% of the value of your portfolio. However, share account fees are capped at £45 per year. Funds are charged at 0.45% for the first £250,000. There is no charge for buying funds, but shares are charged at £11.95 per deal or £5.95 if you do over 20 deals per month. Automatic Regular Investing The latest research from Hargreaves Lansdown highlights just how important it is to invest in an ISA as if you invested your full allowance (£20k) in a stocks and shares ISA over ten years, a basic rate taxpayer could save £8,521 in tax, a higher rate taxpayer £19,336 and an additional rate taxpayer £21,358. Joseph Hill, a senior investment analyst, Hargreaves Lansdown: said that“Albert Einstein called it the eighth wonder of the world, and compound interest has something in common with other wonders of the world – to most people it’s mysterious and beyond comprehension. We asked people what they’d end up with if they invested £10,000 for a year, and their investments grew at 8%, compounded daily. Just 28% of people got the answer right. The most common answer was £10,800 – which is 8% growth without compounding. The actual answer was £10,832. Hargreaves Lansdown suggests that people reinvest their stocks and shares ISA profits in income funds like Artemis Income and Fidelity Global Dividend funds. Becuase income funds are not just for those needing an income today, they can be a great way of seeing compounding in action if investors reinvest the income. This can increase the number of units held in the fund, growing the value of an investment and repeating this process over a long period can be a great way to grow capital. Pros

Cons

Overall4.9 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0.12% |

Dealing Commission 0.08% |

See Offer Capital at risk |

Features:

|

Saxo Stocks & Shares ISA Review: Low costs and direct market access investingDoes Saxo have an ISA and is it better than IBKR's? Yes, Saxo does have an ISA and it is better than Interactive Brokers’ ISA (for some things but not everything). For instance, Saxo’s ISA is cheap, but IBKR’s is free. But, Saxo has better customer service, which in my mind is very important. It’s a close call between IBKR and Saxo, but overall I’d say as the services the two brokers are so similar, IBKR has the better ISA purely based on the price differential. Fees: Saxo Markets charge a custody fee of 0.12% for an ISA. when you buy and sell shares Saxo Markets charges a commission based on a percentage of transaction size. They are very competitive though and UK shares trading commission starts at 0.1% (£100 if you buy £100,000 worth of stock) and drops to 0.05% for more active traders. Special Offers:

Pros

Cons

Overall5 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0.15% |

Dealing Commission £0 |

See Offer Capital at risk |

Features:

|

Dodl Expert Review: A great way to start investing for less.Is Dodl a good investing app? AJ Bell Dodl is a great way for the next generation of investors to invest with a “low-cost, little effort” app which focuses on making investing easy. Which it does well, Dodl is very user-friendly, has great educational content and is one of the cheapest ways to start investing. Pros

Cons

Overall4.3 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees £120 |

Dealing Commission £0 |

See Offer Capital at risk |

Features:

|

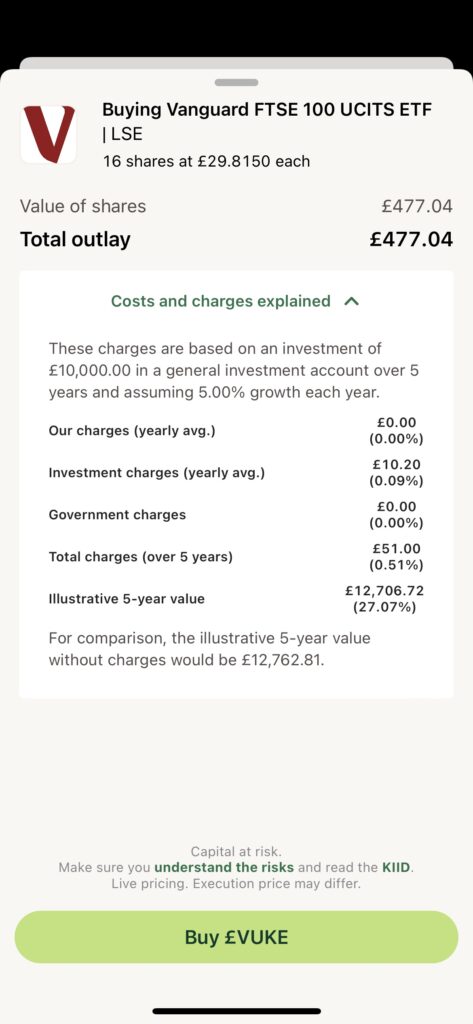

CMC Invest Lets You Invest in Major Shares, ETFs and Funds with No Commission. A Great Way to Get Started.Provider: CMC Invest Verdict: A great investing app for beginners, CMC Invest offers SIPPs, a flexible stocks and shares ISA, a cash ISA with great interest rates and general investment accounts where you can invest in 3,500+ US & UK shares, 400+ ETFs and investment trusts, and 1,000 mutual funds. The Core plan offers £0 commission and FX fees of 0.99%. Is CMC Invest Good for Investing? Yes, CMC Invest is commission-free and gives you access to the most popular UK shares, US stocks and ETFs – a bonus for traders who want to also build a long-term investment portfolio. I tried it out for this review. What is CMC Invest?It’s an investing app that lets you invest for free on major markets. Is CMC Invest trustworthy? Yes, CMC Invest is regulated by the FCA (Financial Conduct Authority) in the UK. CMC Invest is owned by CMC Markets, a FTSE 250 company traded on the London Stock Exchange and worth £726m (as at 12/6/25). Is CMC Invest Safe?Your money is generally safe with CMC Invest as clients’ money must be kept separately from the firm’s money and assets, under FCA rules. But it’s worth knowing that deposits in its cash ISA aren’t protected by the Financial Services Compensation Scheme (see below). CMC Invest lets you invest in the stock market for long-term capital gains, as opposed to its owner, CMC Markets, which lets you speculate in the short-term through CFD trading and financial spread betting. What Can You Invest in with CMC Invest?Since launch in the UK in 2022, the platform has increased the number of UK stocks from 100 to over 500 UK shares, 3,000 US shares and around 400 ETFs and investment trusts. Under its Core plan (which has no monthly fee), you can access over 4,600 global stocks and ETFs. The Plus (£6.99 a month) and Premium (£10.99 a month) plans offer over 6,100. It’s still a relatively small universe of potential investments when you compare it to incumbent DIY platforms like Hargreaves Lansdown and interactive investor, but it’s catching up. CMC Markets has always excelled in building excellent in-house tech for traders to speculate on the most liquid and popular markets cheaply. And in reality, most of the volume that goes through trading platforms is in the top 10 traded assets like the FTSE, Lloyds shares, and EURUSD. Having loads of peripheral markets is great, but actually, all people want is to trade and invest in is what everyone else is trading and investing in. When I opened an account with CMC Invest, it took less than a minute to get up and running and fund it with £500 to get started. Obviously, this was helped in part by the fact that it links to my existing CMC Markets account, reducing the need for additional checking on my identity. There’s a general investment account, a stocks and shares ISA and a SIPP. You can also choose to invest by shares or amount, but unlike other investing apps where you can choose to buy £100 of something through fractional shares, CMC Invest rounds the purchase down to the nearest amount of whole shares. This was a shame because for this review I was going to try and buy the 5 ETFs that our man Jackson Wong suggested were all you need to build a globally diverse portfolio including the FTSE, a world ETF, gilts, property and gold. But of those he suggested, not all were available on the app. So in 2 different ways, I couldn’t just buy £100 of each. So instead, I backed Britain and bought £500 worth of an American-owned ETF that tracks the performance of the FTSE 100 (VUKE). How Much Does CMC Invest Cost?It’s free to invest with a CMC Invest Core account, which includes a flexible cash ISA, interest on univested cash and access to research tools. The FX fee is 0.99% . The Plus account has a £6.99 per month subscription fee, but includes the stocks and shares ISA, a wider range of stocks and ETFs, a higher rate of interest on univested cash and a lower FX fee, at 0.5%. The third option, Premium, is £10.99 a month. For this, you get the SIPP thrown in, along with everything in Plus. Premium gets you the highest rate of interest on uninvested cash and the lowest FX fee at 0.39%. Thankfully, for those getting started, Meridyth Park, former Head of Marketing for CMC Invest, told me there will always be a free version. But as with all investing, there are other costs involved. For example, when I bought those 16 shares in the Vanguard FTSE 100 UCITS ETF, there were no charges levied by CMC Invest, but you still have to pay the Vanguard investment management fee, which is what Vanguard charges for providing and managing the ETF. There is no way around these fees with any investment app, for that particular ETF the cost was 0.09% (£10.20 a year which is £51 over a 5-year period).

It’s really good to see CMC Invest display these charges on the dealing ticket, because most investing apps I see hide this in the small print somewhere or do not really explain exactly what it is. It’s handy to see the fees calculated over a 5-year timeline as well, as that is the average time most investing accounts expect to see people invested for. CMC Invest’s FX fees (when you convert GBP into USD) are fairly competitive – not as cheap as Trading 212 which charges 0.15%. It’s an important charge to be aware of, though, because US stocks are a massive gateway for new investors as they have had stellar returns, and are all over social channels, and are all household names so lots of those starting out investing will dabble in the US markets. The likes of Lloyds and Vodafone, don’t quite have the same appeal as investing in Netflix and Tesla (NASDAQ:TSLA). How does CMC Invest Compare to Other Investing Apps?CMC Invest has great tech, but at the start, it felt that this app was a little rushed out. I know there is a massive race between trading platforms to offer longer-term investing products, but I was quite surprised initially to see such a basic app on offer and no web version. I’d have much rather seen the exceptional trading platform offer the ability to buy and sell physical versions of the assets that can be bought as a CFD or spread bet. I think Saxo Markets does this best as everything is all in one place and when you look at a market you can choose to trade as a future, a CFD or a physical share. IG also does it where you get the same app and desktop platform, but you log in to a share dealing account rather than the trading platform. But CMC Invest told me it hasn’t just been built to cross-sell to traders already signed up, it’s there to target an entirely different audience of long-term investors. Freetrade has better functionality and more markets but in my mind, Freetrade is too early stage to put any proper money into. It seems to have grown too quickly and it makes me nervous. I’d prefer to invest through an app like CMC Invest which is backed by an already established, profitable and publically listed company (CMCX on the LSE). Compared to the robo-advisors like Nutmeg and Wealthify, CMC Invest is much cheaper. If you are confident enough to pick your own investments, you can save in fees. For example, if you have £10,000 on account, that is only £60 a year, but as your account grows, if you have £100,000 invested then that is a massive difference of £3,000 over 5 years. If you’ve got the time and inclination you can just take a look at any robo-advisor’s ETF portfolio and replicate it for free. You do not of course get the benefit of the portfolio being managed or rebalanced on your behalf, though. For a while, zero commission brokers were seen as a marketing gimmick, but now as major brokers like Interactive Brokers look to compete in the free investing market, the bigger platforms have all moved to embrace low-cost longer-term investors. Should You Invest with CMC Invest?I believe it’s good value. If you have a trading account with CMC Markets, the CMC Invest app is a great place to start building your long-term investment portfolio. CMC has always innovated, always been at the forefront of its industry, and always listened to client feedback. Read CMC founder Peter Cruddas’ biography or interview with us, and you can see there is a huge passion for developing great products. He told us back in 2018:

Before writing this review, I also got the chance to talk to Alister Sneddon, who was the Head of Product, and it’s quite clear that he too had a passion for the app. Plus having previously worked with AJ Bell on the Dodl app, Moneyfarm and interactive investor, he had some fairly valuable insider knowledge on what makes an investing app work. So, if you want a feature added, sign up to the CMC Invest forum through the app and say what you want. You never know. You could have a hand in creating the investing app you always wanted where you can also deal for free… Pros

Cons

Overall4.3 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees 0% |

Dealing Commission £0 |

See Offer Capital at risk |

Features:

|

Lightyear Stocks & Shares ISA Review: Zero commission and low FX fees keep US stock investing cheap Account: Lightyear Stocks & Shares ISA Description: Lightyear’s stocks and shares ISAs are flexible, meaning you can move money freely in and out without losing any of your annual allowance. They also have no minimum deposit, and zero commission fees. Overall, Lightyear’s Stocks & Shares ISA remains one of the best value options for cost-conscious investors who want simple, flexible and low-fee global investing. Capital at risk. The value of your investments can go down or up. Is the Lightyear Stocks & Shares ISA Any Good? Lightyear won our 2025 Award for Best Stocks & Shares ISA because it offers a genuinely low-cost, no-nonsense investing experience. Its ETFs are commission-free, the app has excellent built-in research, and the platform remains highly competitive for international investing. Lightyear has now fully removed commission fees for US, UK and EU stocks, strengthening its position as one of the cheapest ISA providers in the UK. In most respects, the Lightyear Stocks & Shares ISA compares very well with longer-established competitors thanks to its transparent pricing. There are no platform fees, no custody fees, no transfer fees and no hidden charges. Trading US, UK and EU shares and ETFs is commission-free, with only stamp duty and fund manager fees applying where relevant. This makes the Lightyear Stocks & Shares ISA one of the cheapest options available. By comparison, the UK’s most widely used investment platform, Hargreaves Lansdown, charges up to 0.45% per year on assets. Vanguard, a lower-cost alternative, charges a £4 monthly account fee for portfolios under £32,000 (equivalent to £48 per year) and 0.15% annually above that level. Lightyear’s pricing advantage is reinforced by research commissioned from Capital Economics, which estimates ISA investors lose more than £850 million per year to account fees. The study found Lightyear’s ISA could be around 10 times cheaper than the average provider over 10 years and up to 16 times cheaper over 25 years. While buying and selling stocks and ETFs and is commission free, investors should remember that ETFs and funds still have their own underlying fund charges. Currency conversion costs 0.1% when converting between GBP and other currencies. Lightyear is still a newer entrant to the investment platform market, which may make some investors more comfortable with longer-established providers. However, it now offers a broad range of investments, including more than 6,5000 US stocks, UK and EU shares, ETFs, money market funds and fractional shares. One area that has improved significantly is cash returns. Investors can now hold money in Lightyear Vaults within the ISA, which invest in BlackRock money market funds and currently offer around 3.75% AER with easy access and no minimum or maximum deposit limits. These variable-rate vaults follow Bank of England overnight rates and provide a competitive way to earn interest on uninvested cash inside the ISA. Pros

Cons

Overall4.7 |

||

|

GMG Rating |

Customer Reviews |

ISA Annual Fees £0 |

Dealing Commission 0.05% |

See Offer Capital at risk |

Features:

|

Interactive Brokers Expert ISA Review: One of the cheapest and best all-round investment ISAsAccount: Interactive Brokers Stocks & Shares ISA Description: Interactive Broker's ISA lets you invest in a huge amount of UK and international stocks and funds with no account charge and very low dealing commissions. It is also has one of the cheapest FX rates in an ISA for investing in US stocks. Is Interactive Brokers' ISA any good? When you think of IBKR, you don’t really think about ISA, but you should because Interactive Brokers’ has one of the best DIY Stocks and Shares ISA around. But why haven’t you hear of it? Well Interactive Brokers is, I would say, at heart, a trading platform for active traders. This is its pedigree and it is one of the best, if not the best trading platform. There is a plethora of apps and platforms that cater to hedge funds, wealth managers and high-frequency active traders scalping the market or trading the divergence between two stocks. Now obviously, if you are investing in an ISA, your goal is probably to try and invest for the long term and achieve capital growth (stocks and funds going up) without taking on too much risk rather than day trading. So, on the surface, IBKR’s ISA doesn’t look like the right fit. But you’d be wrong. Because one thing that active traders and hedge funds need is efficiency, and efficiency comes from low costs. And, as well as colossal market access, one thing Interactive Brokers does really well is pricing. IBKR are one of the cheapest accounts for traders. This, by logic, filters down into their investment accounts. The key difference being that investment platforms like Hargreaves Lansdown, AJ Bell and Interactive Investor charge annual fees for having an account with them. IBKR does not. When I interviewed the IBKR UK MD Gerry Perez, I asked them how they could be so cheap. He simply said they like scale, they automate and that innovation and tech are key to their success – plus, being big means that you can achieve economies of scale (the more you do something the cheaper it becomes). And ultimately, the cheaper they can be the more customers they can win, and the lower their costs can be. It’s a numbers game. To give you an example of how cheap IBKR’s ISA is, here is a breakdown of the costs compared to other stocks and shares ISAs: Account fees: IBKR’s ISA account fees are £0. Now for context, Hargreaves Lansdown charges 0.45%, so if you have £100,000 invested in funds in your ISA, you will save £450 a year with IBKR compared to having an ISA with HL. Or over a five-year period (what people assume a good timescale for ISA investing is) you’ll save £2,250 Commissions: This is the fee charged everytime you buy and sell something. If you want to buy and sell individual stocks instead of buying diversified funds in the hope of beating the market yourself, AJ Bell charges £5 per deal, whereas Interactive Brokers charges £3. As a side note, there are some providers like Freetrade and Lightyear that are cheaper, but they are fairly new providers and not as established (which brings it’s own level of risk). So, if you were to buy or sell shares five times a month for five years, it would cost you £900 with IBKR, but £1,500 with AJ Bell. FX fees: This has a huge impact on investments because it is the hidden cost of buying US shares. Now, as people mainly invest in the US because UK stocks are boring and nobody is interested in investing in Lloyds, but everyone wants to buy Apple shares, it’s very important to understand how much this will cost you. IBKR only charges 0.03% for currency conversions and you can choose when to do the deal, giving you great control over the exchange rate. Compare this to Interactive Investors’ 1.5% for deals less than £25,000 and you can see where this is going can’t you? Buying £10,000 worth of Tesla will cost you £150 in FX fees with ii, but only £3 with IBKR. If you build up £100,000 worth of US stocks in your ISA over 5 years you’ve have paid £1,470 more in FX fees with II versus IBKR. Interest on account: Sometimes you may think the stock market is going to go down and if you don’t want to start hedging the market by shorting stocks, one of the best ways to protect you profits against a market crash is holding cash on account instead of stocks or funds. As interest rates are quite high at the moment, brokerage platforms (after being ticked off by the FCA for not doing this before) now offer interest on uninvested cash. At the moment, if you have over 10,000 USD worth of cash on your account you can get up to 4.33% on that, which is pretty much in line with some of the best-paying savings accounts out there at the moment. Market access: One final point, you can invest in a huge range of bonds, stocks, ETFs and funds. To the point where if you can’t find it on IBKR you probably won’t be able to find it else where. Specifically, as of February 2025, UK investors can now buy mutual funds through IBKR in their ISA account. Those much cheaper apps like Freetrade and Lightyear offer access to the main market stocks, but if you want to invest in something more exotic, you can’t. How does the Interactive Brokers’ Stocks and Shares ISA compare to the competition? Interactive Brokers’ new ISA will need to compete with a host of similar products offered by established providers so who looks the best bet? Following Interactive Brokers’ recent rationalisation of their UK and European commission rates it’s hard to imagine that they can be beaten on trading costs, but what about other fees and charges? Well, Interactive Brokers will charge an activity fee of £3.00 per month, per Stocks and Shares ISA. However, if you generate £3.00 of commission in that month no fee is payable and if you generate a commission of less than £3.00 in a month then the difference between that sum and £3.00 is payable. For comparison, Interactive Investors charges a £9.99 per month ISA account fee and Hargreaves Lansdown charges 0.45% of the value of the ISA, up to a maximum of £45.00 per annum. Whereas at a wealth manager Moneyfarm you can expect to pay an ISA fee of 0.75% of the value of the ISA every month. Interactive Brokers will allow one free withdrawal per ISA, per month and will charge a £7.00 withdrawal fee thereafter. Whereas none of the other providers in the Good Money Guides Stock and Shares ISA comparison tables charges exit fees for cash withdrawals. Pros

Cons

Overall4.9 |

||

|

|

GMG Rating |

Customer Reviews |

ISA Annual Fees £96 |

Dealing Commission £0 |

See Offer Capital at risk |

Features:

|

IG Stocks & Shares ISA Expert Review: A Great All Round Investing AccountAccount: IG Stocks & Shares ISA Description: IG offers an excellent ISA if you want to invest in shares, ETFs and pre-made portfolios in a tax-free wrapper. Investors looking to optimise their 2025/2026 ISA allowance can also get up to £200 or 1% cashback on deposits made before 5 April 2026 if they open an IG ISA account before 13th February 2026. Capital at risk. Is IG A Good Stocks & Shares ISA Account? Yes, if you want to invest in shares, ETFs and pre-made portfolios in a tax-free wrapper, IG offer a stocks and shares ISA. If you want to combine your short-term trading with some longer-term investments, you can have both on IG. If I’m completely honest, there are better stand-alone investment platforms that offer ISAs like Interactive Investor, where you pay a flat fee for all your accounts as opposed to IGs quarterly custody fee. But for tax-free trading (spread betting) and tax free investing (ISAs), IG has a very good offering. Fees: IG has removed dealing fees so you don’t pay commission when you buy and sell UK or US shares in your ISA. IG charge £24 per quarter in custody fees for an ISA account, but this is waived if you trade at least 3 times per quarter. Smart Portfolio fees are 0.5%, capped at £250 per year. Fund management charges are 0.13% and transaction costs are 0.09%. IG offer a very cheap way to include US stocks directly in your investment ISA. But, if you prefer not to trade in individual equities you can take advantage of and invest in a range of Smart Portfolios that are selected and managed by BlackRock on IGs behalf. There is zero commission on US stock and UK share trades. Market Access: Brilliant – whenever I am writing a “how to buy shares in…” guide I always check IG first as they have about the broadest range of shares to trade as possible. Fairly limited on investment funds, but they also have Smart Portfolios for investors who want a pre-built managed investment portfolio. App & Platform: Superb, I’ve been using and comparing IG for over 20 years and they have always had and continue to produce some of the best investing apps and platforms. Customer Service: Great if you’re a big customer as you get a personal account manager. I’ve had a few issues trying to phone and get help in the past, but most things can be fixed online. Research & Analysis: IG always produces great research from analysts like Chris Beauchamp, who was in our Quiz of the Year. Plus IG has lots of educational guides and the platform has integrations from Reuters and other news sources. IG’s social channels are worth following too for daily market commentary. Pros

Cons

Overall4.9 |