Use our JISA calculator to show your children how much their money could be worth when they turn 18 if they invest it in a stocks and shares ISA rather than spend it.

It’s important to remember that investments can go up as well as down so past performance is no indication of future performance.

What is this JISA Calculator for?

The JISA calculator helps you estimate how much a child’s Junior Stocks & Shares ISA could be worth by the time they turn 18. It takes into account how much you put in, how long you invest for, and the growth rate you expect.

It shows:

- The final JISA value (the projected pot size at 18)

- The total contributions you made

- The total returns (how much growth came from investing rather than just saving)

How To Use The Junior Stocks & Shares ISA Calculator

| Field | What it means | Notes |

| Initial JISA Contribution | A one-off lump sum at the start | E.g. birthday gift, savings kick-start |

| Expected Annual Returns | The assumed average yearly growth | Default is often 5 %. You can try 3 % (cautious) or 7 % (optimistic) |

| Monthly Contribution | Regular savings you add each month | E.g. £25, £50, £100 |

| Years Invested | How long the account runs until age 18 | If child is 2, enter 16 (to reach 18) |

JISA Calc Step-by-Step Use

Enter an initial contribution (or £0 if none).

- Set your expected annual return.

- Enter how much you’ll add each month.

- Input the years invested (up to 18 total).

- Click calculate to see: Final Value, Total Contributions & Total Returns

You can adjust the numbers to compare scenarios (e.g. £25/month vs £100/month, or 4 % vs 7 % growth).

Key Things to Know About Our Junior Stocks & Shares ISA Calculator

Unlike Junior SIPPs, JISA money becomes accessible at 18, not locked away until retirement.

The annual JISA allowance (2025/26) is £9,000 per child — you can’t contribute more than this each tax year.

Growth and withdrawals are tax-free.

The calculator does not include fees (fund charges, platform costs).

A Real World Example Of How Much A Junior Stocks & Shares ISA Can Generate

Say you open a JISA for your child at birth with:

- £1,000 initial contribution

- £100 per month

- 7 % annual returns

- 18 years invested

By the time they turn 18, the calculator shows:

- Total Contributions: £22,600

- Final JISA Value: ~£38,700

- Total Returns (growth): ~£16,100

So your £22,600 of savings could potentially turn into nearly £39,000, completely tax-free, giving them a strong financial head start at adulthood.

Ready to open a Junior Stocks & Shares ISA?

You can compare the best JISA accounts using our Junior stocks and shares comparison table below:

| Name | Logo | GMG Rating | Customer Reviews | JISA Annual Fees | Dealing Commission | CTA | Tag | Feature | Expand | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

GMG Rating |

Customer Reviews |

JISA Annual Fees 0.5% |

Dealing Commission £0 |

Award Winner 🏆 |

Features:

|

Beanstalk Investing App Expert Review: Voted Best Junior ISA 2026 Provider: Beanstalk Investing App Verdict: Beanstalk is an investment app that helps you invest for your children through a Junior ISA. It was founded by the team behind Kidstart (a cashback site for children's shopping) and won "best Investing Account" in 2025 and in 2022, 2023, 2024 & 2026 the award for Best Junior Stocks & Shares ISA as they make setting up an account to invest for your children's future cheap, easy, flexible and accessible for you and for others to contribute to. Is Beanstalk a good investing app? Yes, Beanstalk won best investing account (as voted for by customers) in the 2025 Good Money Guide Awards. Beanstalk is a super simple way to start investing in an ISA. You can either invest as an adult of in a Junior ISA for your children, which you can split between cash savings and the stock market. Beanstalk Junior Stocks and Shares ISA Beanstalk has won “Best Junior Stocks and Shares ISA” in our 2024, 2023 and 2022 awards. They offer one of the easiest ways to invest for your children and you can quickly move money between cash and the stock market to manage the amount of risk/reward you want to take. Julian Robson, founder and CEO of Beanstalk said after winning the award: We’re thrilled to have won the Best Junior ISA Award from the Good Money Guide Awards for the third consecutive year. It’s a fantastic recognition, reflecting our unique and valuable proposition for parents and grandparents who want to invest in their children’s future. Our focus is on encouraging long-term investment over cash savings, as that tends to yield better returns. We aim to support first-time retail investors with a simple solution to put money away for 18 years, and it’s great to see the UK retail investment market thriving. Beanstalk provides a simple yet effective way to invest for your children’s future. Friends and family can also make deposits directly into your child’s account via the app. The investment options are split between cash and the stock market enabling parents to adjust the level of risk they are prepared to take. It’s a good option for parents who want to investment for their children, but don’t want to pick individual investments. Why is Beanstalk so good? Well… We quite often go to the ponies as a family, and if there is more than a single page of horses on the card for a race we always let the children have a little bet to cover more of the field. A while ago we were at Sandown, it was the last race of the day, and Hugo, my youngest, chose a horse based on the only sensible strategy available to a two-year-old, he picked one at random. As luck would have it, it was a rank outsider, a 13-year-old with an exceptional track record that was now a little bit long in the tooth. But, he wished and he hoped and Wishing and Hoping romped home to win at 50-1, after leading the pack the entire race. ITV Racing caught us trackside on the TV as the owner burst into floods of tears and the trainers were whooping away. That’s us on the left clapping the trainers…

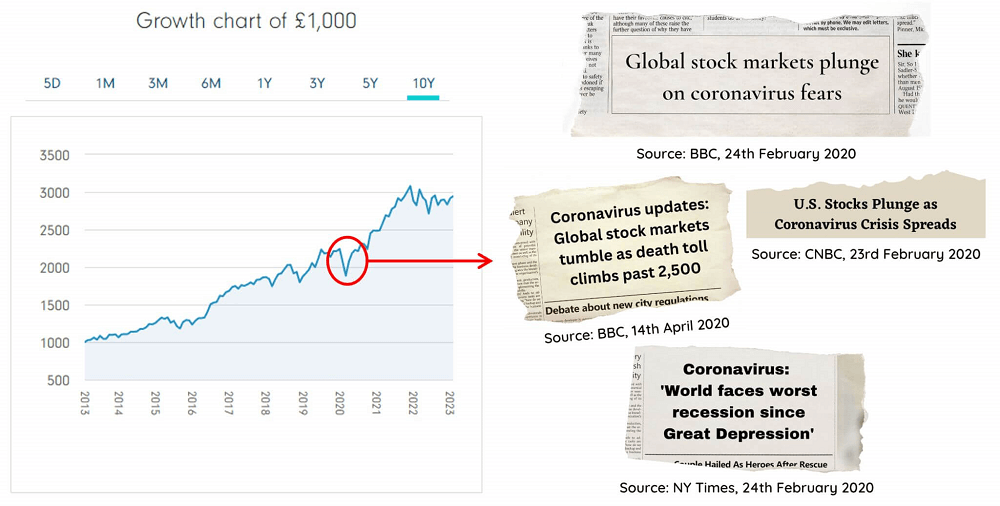

We didn’t get 50-1, we got 34-1 because we only bet with the bookies at the track, in particular, we like a chap called Barry, who wears a Fedora. A tidy return nonetheless, but what to do with it? Usually, we’d all go out to dinner to celebrate, but because it was Dry January, we just went home. And because we’re trying to be more responsible parents, we thought we’d invest his winnings. Let it ride as it were, on the biggest bet out there, the stock market. Previously, we invested one of my other children’s birthday money through GoHenry, but as Hugo is too young to get pocket money, I chose Beanstalk for him. But was it a good time to be investing in your children’s future? I hear you ask. The stock market was coming off five-year highs, we may have been in a recession, the world is nearly at war and the tech giants who have historically created massive shareholder returns are laying people off left right and centre. Well, here’s the thing, there is always a disaster around the corner, and actually now is the best time to start investing, because it is in fact, now. When it comes to long-term returns (Hugo can’t access money in his JISA until he is 18), the best time to invest is as soon as possible. When I interviewed Julian Robson, the co-founder of Beanstalk, he told me that one of the inspirations for setting up the Beanstalk JISA was a chart that was on the wall in his old boss’s office. It was a chart of the stock market going back to the 1900s. His point was that if you look at a long-term chart of the stock market, you can’t see 1987’s Black Monday, The 1930’s Great Depression, or any other major stock market crash. In general, it just goes up. Here is a good example of the Covid market crash that Cem Eyi (Beanstalks other co-founder highlighted on LinkedIn recently (the fund is Fidelity World Index).

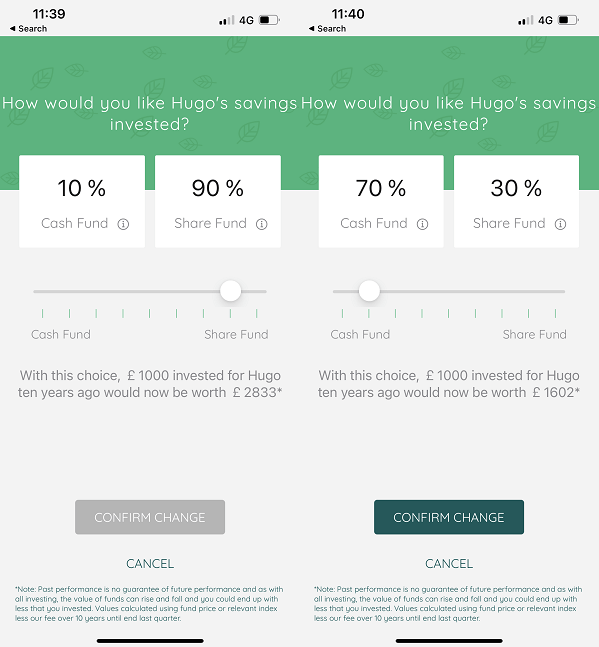

What does Beanstalk invest in? When you invest in a Junior stocks and shares ISA with Beanstalk, you are essentially making two investments (three if you want to include your child’s future), the Legal & General Cash Trust fund and the Fidelity Global Index fund. The first tracks interest rates and keeps your money as cash, the second tracks the stock market, and holds big profitable companies like Apple, Microsoft and Johnson & Johnson (you can see the full portfolio breakdown here). It’s a standard diversified portfolio. How much does Beanstalk cost? It costs 0.5% of the balance of your portfolio for a Beanstalk JISA, but if cost is your only concern, you can buy these funds individually with a DIY platform like AJ Bell (0.25%) and interactive investor (JISA is free with a £9.99 per month trading account). Regardless of who you invest with, you will still have to pay the 0.12-0.15%. charges levied by L&G and Fidelity for managing the fund. It’s worth noting that Hargreaves Lansdown Junior ISA is now free, so much cheaper. Why invest in a Beanstalk ISA? Where Beanstalk earns its money is that you can very easily switch between what percentage of cash and stocks are in your child’s portfolio. There is a handy slider, which also shows what the historic returns would have been depending on the allocation. So, if you think the market is going to crash, you can switch to more cash and interest, rather than stock market investments. But remember, a general rule of thumb when it comes to investing is that the younger you are, the more risk you should take. If you are old, the closer to retirement you are the lower risk your investments should be. So, when your child comes close to 18, you can tune down the risk so that you don’t get bitten by a shock stock market crash the week before they get their money.

I’m not suggesting for a second that you bet on horses to kickstart your children’s financial literacy, that would be idiocy. But, if you have a few pounds sitting around, pick up your phone, download the app, and start investing for your children’s future. If you’re looking to bet on a winner, that’s a sure thing. Pros

Cons

Overall4.3 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GMG Rating |

Customer Reviews |

JISA Annual Fees £0 |

Dealing Commission £0 |

Features:

|

Hargreaves Lansdown Junior ISA Review : Best Junior ISA (JISA) 2025 Account: Hargreaves Lansdown Junior ISA Description: Hargreaves Lansdown has one of the best JISA as there are no account costs and your money can be invested in the stock market. Hargreaves Lansdown is one of the largest investment platforms in the UK, and have recently removed their Junior ISA fees. You also get the widest selection of UK and international shares as well as bonds, ETFs, VCTs, gilts and bonds to invest for your children. Is the Hargreaves Lansdown Junior Stocks and Shares ISA any good? Yes, Hargreaves Lansdown won “Best Junior Stocks & Shares ISA 2025” in the Good Money Guide Awards. Since Hargreaves Lansdown removed the fees from of its JISA (Junior ISA) account it is now one of the cheapest ways to invest for your children.. This is good news as Hargreaves Lansdown is generally acknowledged to be not only the largest provider of direct-to-consumer investment services but also the most expensive. As well as seeing record inflows in 2024 for the now free junior ISA investing account, HL also reports that over one-third of JISA are paid into every month and that the average account value of a junior stocks and shares ISA when it converts into an adult ISA is £18,829. The Junior ISA is aimed at those under the age of 18 and is designed to encourage long-term saving on behalf of children and teenagers. Those goals have received a boost with Hargreaves Lansdown removing its fees on the Junior ISA. Junior ISAs, which are often managed by parents, grandparents or guardians, on behalf of a young person, will now be able to trade or invest in funds and ETFs, UK and overseas shares, gilts and other bonds, free of charge. If those deals are transacted online or as part of a regular savings plan via direct debit. Charges will still apply if orders are placed over the phone with the Hargreaves Lansdown’s dealing team, or via the firm’s postal dealing service. Hargreaves will also waive charges associated with account opening or closing, transfers of stock or cash, and the production of quarterly statements. Though the firm will retain some credit interest to cover its administrative expenses. UK and Irish Stamp Duty charges and the UK PTM levy will still apply to qualifying equity trades, as will purchase and financial taxes on certain French, Spanish and Italian securities. Hargreaves Lansdown’s biggest rival is AJ Bell, who charge 0.25% on the value of shares held in a Junior ISA, though that fee is capped at £2.50 per month. AJ Bell also has a custody fee of 0.25% per annum and a variable fee schedule for trading. Regular online investments attract a charge of £1.50, as do dividend reinvestments and trades in unit trusts. Online trades in equities, investment trusts, ETFs, Gilts and bonds are charged at £9.95 per trade. Though that can fall to just £4.95 if the account traded 10 times or more in the prior month. Telephone orders at AJ Bell are charged at £29.95 per trade. AJ Bell’s Lifetime ISA charges 0.25% of the value of shares held in the account, capped at a maximum of £3.50 per month. Once again custody charges of 0.25% also apply. Though if an investor is holding more than £250,000 in funds, within their AJ Bell Lifetime ISA, then the custody charge falls to 0.10%. And if they hold £500,000 or more in fund investments there are no custody charges levied. Over the long term, fees can negatively affect the performance of an investment portfolio. So for Junior ISA holders and those that manage the accounts, a no-fee solution is a very positive step. And one that will hopefully encourage parents, grandparents and guardians to invest on their charges’ behalf, and to choose Hargreaves Lansdown as they do so. Which, is no doubt what the no-fee offer is designed to encourage. However, there is no cash Junior ISA at HL. Hargreaves Lansdown only has a stocks and shares junior ISA, but you can receive interest on your uninvested cash (essentially making it a cash ISA). Pros

Cons

Overall5 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

GMG Rating |

Customer Reviews |

JISA Annual Fees £0 |

Dealing Commission £3.99 - £5.99 |

Features:

|

Interactive Investor Junior ISA Review: A Free Self-Select JISA For II Customers Account: Interactive Investor Junior ISA Description: With an ii JISA you can invest in over 40,000 shares, bonds, funds or pre-built portfolios. So if you are looking for a free self-select JISA it is one of the cheapest and most flexible investment ISAs for children on the market at the moment compared other large investment platforms like AJ Bell (who charge 0.25% a year). You also get one free trade per month, after that it costs £5.99 per deal, compared to AJ Bell’s £9.95 per share deal. Is the Interactive Investor junior ISA (JISA) any good? Yes, Interactive Investor’s JISA is a great way to invest for your children if you have an investing account with ii as it’s free and you can invest in a huge range of shares, bonds and funds. If you have an investing account with Interactive Investor, you get a free Junior stock and shares ISAs account for your children. Fees: *II JISAs are free for customers who have already opened an ISA or Trading Account. Dealing commissions are a free trade every month, then UK Shares and Funds, US Shares charged £7.99 or upgrade to a £19.99 “Super Investor” account 2 free monthly trades and deal for £3.99. Regular investing is free. Special Offers:

Pros

Cons

Overall5 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GMG Rating |

Customer Reviews |

JISA Annual Fees 0.75% |

Dealing Commission £0 |

Features:

|

Moneyfarm Junior ISA Review: A Good JISA For Simple Risk-Based PortfoliosAccount: Moneyfarm Junior ISA Description: Moneyfarm smart tech allows you to monitor your JISA’s performance from anywhere, automate your monthly deposits so you’ll never miss an opportunity again, and their team of dedicated investment consultants are on hand to answer any queries you may have via anytime calls, chats, or emails. Can you invest for your children in a Moneyfarm JISA? Yes, the Moneyfarm junior ISA has the same portfolios as the standard GIA, ISA and pension account. So you can invest tax free for when your children turn 18. Fees: Moneyfarm junior stocks and shares ISA account fees are scaled between 0.75% for accounts between £500 and £50,000, then above £100k are 0.45% to 0.35%. Average investment fund fees are 0.2% and the average market spread when buying and selling is 0.10% Pros

Cons

Overall4.7 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

GMG Rating |

Customer Reviews |

JISA Annual Fees 0.25% |

Dealing Commission £3.50 - £5 |

Features:

|

AJ Bell Junior ISA Review: A Well-Rounded & Good-Value Low-Cost JISA Investing AccountAccount: AJ Bell Junior ISA Description: AJ Bell is one of the cheapest self-select JISAs with account fees of only 0.25%, although it is not free. Fees are capped at £2.50 per month for shares, investment trusts ETFs, gilts and bonds, but there is no cap for holding funds. You also have dealing charges of £1.50 for funds and £9.95 for shares. It is more expensive than Hargreaves Lansdown’s (now free) JISA and providers a relatively similar service. Does AJ Bell Offer A Junior ISA (JISA)? Yes, AJ Bell offers a stocks and shares junior ISA where you can invest in the stock market for your children. Fees: AJ Bell charges 0.25% of the value of your for a Junior ISA. Share account fees are capped at £2.50 a month. Dealing costs are £1.50 for funds and £5 for shares but drop to £3.50 where there were 10 or more online share deals in the previous month. Special Offers:

Pros

Cons

Overall4.9 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GMG Rating |

Customer Reviews |

JISA Annual Fees 0.45% |

Dealing Commission £0 |

Features:

|

GoHenry helps kids get investing as well as spending and savingProvider: GoHenry Verdict: GoHenry is an excellent pocket money app that helps children learn about money by giving them the independence to make their own choices about what they spend their cash on. They also have a Junior Stocks and Shares ISA that lets you invest in your children's future. Once you invest in a JISA the money is held in a tax-efficient account and can only be accessed by your child when they turn 18. Is GoHenry any good? GoHenry is a great way to combine educating your children about the future value of money along side giving the financial independence with their pocket money app. When you invest in the GoHenry Junior ISA you are buying Vanguards LifeStrategy 60% Equity Accumulation Fund, which contains a mixture of stocks and bonds. GoHenry’s Junior ISAGoHenry’s Junior Stocks and Shares ISA lets you invest for your child’s 18th birthday in Vanguard’s LifeStrategy 60% fund and can be opened by parents or guardians of kids under 16 who live in the UK. I got quite drunk at the City Am awards the other night, and after Nick Ferrari told some amusing stories about Boris Johnson and made some Whatapps jokes and dinner had been cleared, I found myself aimlessly wandering around looking for someone to talk to. The same thing happens to me at conferences, it reminds me of nightclubs at university or Saturday night discos at school pretending to look for the loo. I really just wanted to go home, but before I did, I was delighted to see that Louise Hill, one of the founders of GoHenry, who won “Entrepreneur of the year”, was still at her table. So I strolled on over, didn’t introduce myself, and started waffling about how GoHenry was one of the best apps in the world, anywhere, ever. I’ve been chasing an interview with GoHenry for a while now, as it’s always nice to hear from the people who set up these game-changing apps to see what makes them tick. Will Carmichael, who founded Rooster Money (before Natwest bought it), had some great stories about trying to predict the stock market based on what children spend their money on. Julian Robson from Beanstalk, also had some fascinating insight into why there is never a bad time to start investing, particularly the key advantage children have over adults when it comes to investing, that being time in the market, rather than timing the market. Anyway, it was a brief encounter, and hopefully, we’ll nail them down for a proper chat at some point. I’m glad I did though because GoHenry has genuinely changed our lives as parents. It would be hard to say that about most financial apps, becuase they are all basically just tools. But what GoHenry has done is made our lives cheaper and easier and that’s a big win. We first started using GoHenry during lockdown, so that the children could earn money for doing chores, but that actually became a bit of a chore for us because if I’m completely honest the app itself is a bit slow, takes ages to log in and the UX is a bit tricky to navigate. So we fairly swiftly stopped allocating pocket money based on chores and now the children just get a regular £5 a week. The issues with the app aren’t such a big deal because they never use it, but love their cards. Amazingly they always know where they are, and haven’t lost one yet. I’d say I login once a month, so I can cope. But, more importantly, it’s revolutionised our children’s attitude to asking for things. Before GoHenry every time we went anywhere, ever, we would be pestered for tat in gift shops, sweets in the supermarket and pleas for things their friends have. Sometimes we’d give in, and it would cost us a fortune. But now, if they want something, we just say, “of course, you can have it if you buy it yourself”. Which triggers children to think about whether or not they actually need something. Or, if they want it more than they want something else because unlike (in their eyes anyway) their parent’s unlimited supply of magic money, being able to see what they can afford and if they buy this they may not be able to buy something else, makes them think twice about what they want. So it’s made our lives easier because we’re not asked to buy so many unnecessary things. Despite raising the cost of having the pocket money card from £2.99 to £3.99 a month and in percentage terms of their account balances that is massive, it’s worth every penny because we are certainly spending less than that overall. In fact, we hardly buy them anything, they do it themselves. GoHenry can even make you money, well not you, but your children. If you get them investing with a JISA (for an additional 0.67% a year). The key advantage of investing in a Junior ISA for your children is that once the money is in, it’s in and you can’t take it out. In fact, only your child can withdraw it when they are 18, and all profits are tax-free. Some may argue (Justin Urquhart Stewart did when I interviewed him) that 18 is the worst possible time to give children any money because they are so irresponsible at that age, but then they must grow up and make their own mistakes. Is the GoHenry JISA safe? Yes, your funds are invested with Vanguard which is regulated by the FCA and protected by the FSCS. What happens to the GoHenry JISA at 18? At 18 Junior ISAs automatically turn into adult ISAs and your children are free to withdraw their money. Interest Rates & ReturnsThe main disadvantage of course, is that stocks and shares ISA can go down in value, which ours actually have. So, the GoHenry Junior ISA doesn’t pay interest, instead, it makes money based on how well the stock market performs. But that’s fine because we’re not trading in the short term, that money will be locked away for a good few years in Vanguard’s LifeStrategy 60% fund, which is one of the cheapest and most diverse funds about. The 60% represents the fund’s exposure to main market stocks, which generally go up. The 40% is in bonds, which generate steady income. What’s also good about the Junior ISA is that if our children want anything ridiculous, we can force them to invest. For example, my daughter has been begging for a pair of Air Jordans which we’ve always said no to because they are over £100 and it’s insane for an eleven-year-old to have shoes that expensive. So what we actually did was buy her a second-hand pair on eBay as a treat for dealing with the stress of finding out from Surrey Country Council what school she has been allocated. However, even though we bought them, we deducted the £69.74 from her pocket money and transferred it to her JISA. Because, whilst your children will grow out of shoes, what you really want to see grow is their financial independence so they have enough money to travel the world on their gap year. What does the GoHenry JISA invest in?When you invest in the GoHenry JISA, you are buying the LifeStrategy® 60% Equity Fund – Accumulation fund, which is a fund invested in 17 different other funds that track various stock and bond markets. 60% of the fund is in equity funds, whilst the remainder is in fixed-income products such as bonds. The breakdown at the time of writing is:

How much does the GoHenry Junior ISA cost?The GoHenry Junior ISA costs 0.45% per year, based on the value of your child’s account. There is also a 0.22% fee charged by the fund manager, Vanguard. You also need to pay the £3.99 pocket money app monthly fee. The annual fees are the same are Hargreaves Lansdown, but more than AJ Bell’s 0.25% (although you do have to pay £1.50 when you deal). Interactive Investor are also a cheaper option if you just plan on buying the same Vanguard fund once a month as their JISA is free with an adult trading account and you get one deal a month free (after that it costs around £5.99). Alternative Junior ISA (JISA) Accounts

Who owns GoHenry?GoHenry was recently acquired by rival platform Acorns and as is often the case in these situations it looks like the new owners are reviewing their acquisitions pricing structure. GoHenry Co-founder and COO, Louise Hill, was recently asked about the tie-up with Acorns and the values of their new parent company which she said was to ensure the financial wellness of the everyday American by encouraging them to start investing early in a non-invasive way. GoHenry was founded on the premise that educating children about money and personal finance was a societal good so their values seem to be aligned. Together, Acorns and GoHenry have nearly 6 million subscribers globally (across five countries).” However, Louise Hill seems keen to move beyond just offering services to young people and would like to expand the franchise to include the over-18s. Now that they have been bought by the Americans, GoHenry has announced a price rise for its subscribers, who will now have to pay 33% more each month to use the pocket money app’s pre-paid debit card. GoHenry, the savings and debit card app focused on children and teenagers, has announced an increase in the subscription paid by its users. Subscribers will now have to fork out £3.99 each month to use the pocket money card. That may not sound like a lot but it represents a +33% increase over the previous monthly charge of £2.99. Price rises post-acquisition are not confined to GoHenry, Nutmeg which was acquired by JP Morgan raised fees under its new ownership. However, Roostermoney, which was bought out by Natwest, recently scrapped a proposed £1.99 per month subscription fee for access to its pre-paid debit card and pocket money app. The monthly fee was to have become applicable in May. The new owners relented on the charge, if only for NatWest Group customers, including RBS and Ulster Bank account holders. Clients at other banks can still use the Roostermoney app and pre-paid debit card, but they will have to pay a £1.99 per month fee to do so. Roostermoney was launched in 2016 and the app allows parents to load pocket money onto a pre-paid Visa debit card, which can be instantly frozen if it’s lost. Parents can also block payments to specific merchants and the app provides real-time spending and balance notifications to both parents and children. Kids spending habits on pocket money appsThe Good Money Guide’s Jackson Wong, recently wrote about Roostermoney’s Pocket Money Index, which tracks the spending habits of more than 125,000 young people, asking could the index help us to predict stock market moves, you can read it here Educating youngsters about money and personal finance is a very good idea and one that will help them no end in later life, when managing your finances, saving and investing for the future becomes increasingly important. Seeing those juveniles as cash cows, however, is another thing entirely. Hopefully, stiff competition between providers will keep such price rises to a minimum. Hargreaves Lansdown, the country’s largest direct-to-consumer savings and investing platform, recently removed trading fees within its Junior ISA, for example. Pros

Cons

Overall4.7 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GMG Rating |

Customer Reviews |

JISA Annual Fees 0.6% |

Dealing Commission £0 |

Features:

|

Wealthily Junior ISA Review: Invest In A Managed JISA From Just £500Is Wealthify's junior ISA ethical or risky? It’s both! When you invest in a junior ISA through Wealthify, you have the choice of an ethical investment plan. But as you are investing in ethical elements of the stock market, there is a risk that the value of your child’s portfolio could go down. Fees: It costs 0.6% to start investing in a junior ISA with Wealthify, which is one of the cheapest robo-advisor general investment account fees. There are also investment costs of on average 0.16% for original plans and 0.7% for ethical plans. Special Offers:

Pros

Cons

Overall4.6 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

GMG Rating |

Customer Reviews |

JISA Annual Fees £0 |

Dealing Commission £0 |

Features:

|

IG Junior Stocks & Shares ISA: Take a punt early Provider: IG JISA Verdict: IG's Junior Investment ISA has no account charge and there is no commission charged on investments. Parents can choose from more than 12,000 global shares and exchange-traded funds, to build their children diversified portfolios tailored to long-term goals such as university costs, a first property deposit, or travel. Is IG's Junior ISA Any Good? Overall, we rate IG’s junior ISA as one of the best in the UK with zero commission, no account fee and lots to invest in from an established provider. Pricing: IG’s JISA is essentially free (apart from a few FX charges if you invest in US stocks) so your children’s investments won’t be erroded by excessive fees. Market Access: Huge market range, loads of UK and international shares, ETFs and investment trusts. So well-suited for parents who want to pick and choose what they want to invest in for their kids. When testing the IG JISA, I opened an account for my son, and bought him some shares in IG. I’ve always liked the company and IG Group has done well recently. The recent diversification away from just trading into investments should help the platform scale and grow in the long run too. You can also buy some really cool stuff, like complex ETFs. You obviously shouldn’t take on too much risk with your children’s future, but the younger your are the more risk you can afford to take. Plus, my mate Jackson just tipped Live Cattle on Invesdaq, because cattle herds have stayed stagnant while demand has risen from natural population increase, so I bought him a few pounds worth.

App & Platform: Just like the trading platform, super simple, took me five minutes to set up a JISA, deposit fund and buy some shares. There are two problems, though, which I’ve marked IG’s ISA down slightly because of (otherwise it would have been five stars). For some reason, you can only open a JISA on IG if your child is under 13, instead of 18, so I couldn’t open a JISA with IG for my oldest child, who is 14. Which is a bit unfair on her, so I’ve only used IG’s JISA for a small test trade, as it would be unfair on her if I invested more for the others. Also, you can’t (or I couldn’t see how to) set up recurring orders where you buy shares, funds and ETFs on a regular basis. It’s a really good way to build up investments for your kids on a “set-and-forget” basis. Customer Service: IG always delivers on customer service, never had any problems with them. The chatbot is fine, as when I tested customer support by asking why I couldn’t open a JISA for my child over 13 it did give me the answer fairly quickly. Research & Analysis: IG has great news, analysis and social channels with lots of market commentary that can help you make investment decisions. Pros

Cons

Overall4.9 |