- BP share price steady as global decarbonisation accelerates

- A paradigm shift into a ‘net zero’ world is happening at speed

- BP is highly profitable and not overvalued

- Buy BP shares to bet on a cyclical upswing

BP, short for British Petroleum, is a major oil company listed in the London Stock Exchange (also listed in the US, NYSE:BP). The £87 billion company not only engages in oil exploration, it also refines, markets and distributes petroleum products. Given the utmost importance of oil in modern industrial societies, the ‘business moat’ around oil companies is deep and wide. In the third quarter, BP earns a staggering $8 billion. Mind you, that’s on top of the $8 billion it earned in the previous quarter. And for the last financial quarter of the fiscal year, BP probably earns another $5 billion.

In the oil baron Getty’s immortal words:

“My formula for success is rise early, work late and strike oil.” Because once you find oil, profits just roll in.”

Why is the oil business such an enduring one? For one, there is this international “cartel” called OPEC (for oil exporting countries) that attempts to regulate the price of oil. When the price of oil is low, OPEC members cut the production of oil to restrict market supply. When the price of oil is too high, it causes a worldwide recession. Demand drops, so does the price of oil.

The other point is what the economists called ‘stickiness’. Once industrials and transport systems are run based on petroleum products, it would be very hard to wean them off. Motorists have to keep buying oil to keep their cars running.

So attractive is the oil business these days that even Warren Buffett is eyeing a deal to acquire up to 50 percent of Occidental Petroleum (NYSE:OXY). Many oil stocks are also repurchasing their shares to deliver higher shareholders’ returns.

Moreover, just recently (18 Jan) the influential International Energy Agency (IEA) anticipated that the demand for crude oil could rise to an all-time high of 101.7mn barrels per day in 2023.

However, the oil sector does not always have a rosy outlook. At times, investors have dumped oil stocks when the world was flooded by a gush of oil. This caused oil prices to drop to extreme levels. An example is the $10 per barrel in 1998.

More recently during the 2020 covid pandemic, oil prices even sunk to negative levels ($-37) because all storage tanks were full to the brim and there were no taker for those surplus oil. In these extremely bearish cases, oil stocks plunged.

BP, for instance, slumped from 600p in 2019 to 200p in just 15 months. That’s a drop of 65 percent. Volatile stuffs.

And lastly, we are progressing into a ‘transitioning’ world – from hydrocarbon to net-zero. This movement of decarbonisation is moving at speed. It is only a matter of time before oil is displaced from our industrial societies. As the Saudi oil minister Sheikh Zaki Yamani once said, “The stone age came to an end not for a lack of stones, and the oil age will end, but not for a lack of oil.”

BP does well when oil is in demand

So back to the question of whether BP is a good long-term investment. Yes, if you believe that oil is here to stay for the next decade or so. No, if you think the Oil Age is ending and there could be better bets out there in new energy systems like hydrogen.

Buy the dipstick?

Remember that the oil sector is a highly cyclical one.

When the world economy is humming along nicely, oil price rises. So does BP’s share price. On the contrary, the threat of a major recession will cause oil price to drop. This drags BP’s share prices lower.

So the best time to buy BP’s share price is when the oil outlook is very negative and earnings from oil companies are pessimistic.

On the BP share price chart, there seems to be a long-term price ceiling at around 600p-780p. So investors of the stock may wish to lock in profits at this level.

At the opposite end, I would watch to buy at 300p-250p as there seems to be strong support at this level.

Correctly valued

It all depends on the price of oil.

While oil prices have dropped in the last few months, at $80-85 (brent) they are only back to the level reached in February 2022. This means that BP will continue to report reasonably earnings in the foreseeable future.

Currently, BP’s price-earning ratio is at a lowly 4.5 (as reported by zacks.com). But is BP ‘undervalued’ based on this? We have to dig deeper.

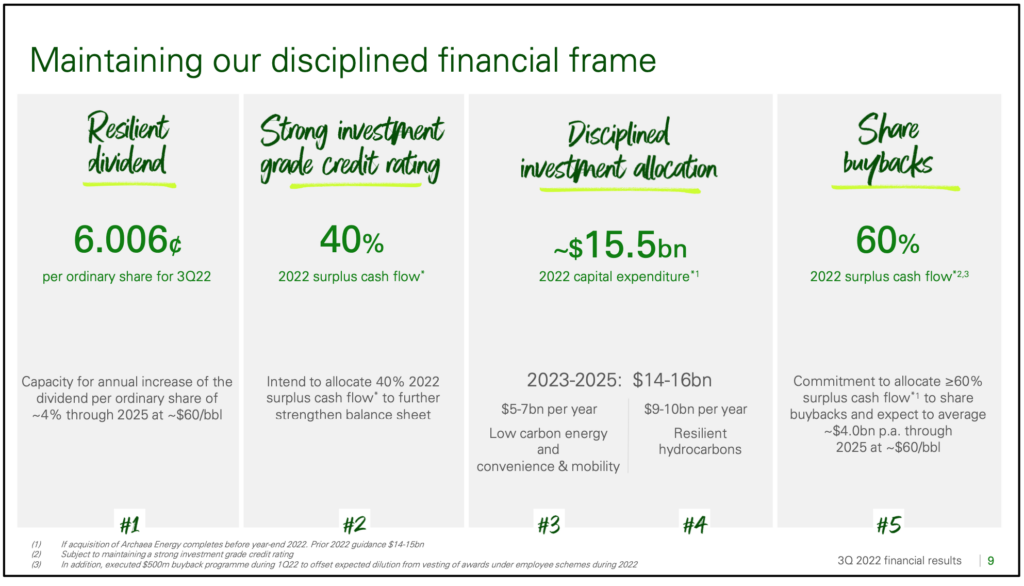

First, BP has net debt of $22 billion. This may be sustainable – as long as oil prices continue to stay elevated. Second, BP is increasing returns to shareholders via buybacks. This is soaking up a lot of available free cash flow (up to 60 percent, see below). Third, BP needs to spend big in alternative energies to tackle the decarbonisation movement.

Overall, I would say BP is rightly valued at this point – neither overly bullish nor bearish based on the available information. Should the market sentiment towards energy change abruptly, then BP shares will move along with it.

Source: BP plc

What moves BPs share price?

BP’s share price depends on two things:

- the general stock market

- the price of oil.

Since October, BP’s share price has been advancing due to these two bullish factors.

- A less negative market sentiment – caused by a change in market outlook on interest rate increases. No longer is the Fed expected to hike rates by 75bps. Now the consensus is 50bps.

- Steady oil prices – which helps to underpin the high level of profits earned by oil majors.

Moreover, with the opening of China, oil prices are now expected to rise as Chinese tourists resume their foreign travelling. With these factors in mind, BP shares have remained steady above 420p.

Predictions & forecasts

With the global economy decelerating, the outlook for oil is a tad more bearish than six months ago. Still, at the current oil prices big oil companies are expected to continue to rake in billions of profits.

BP is a widely-held share. Out of the 25+ analysts who followed the stock, about half recommended ‘Buy/Outperform’. This means that the investment community is expecting BP to retain its ‘high-profit’ mode in 2023.

As for the median price target, it is set at 550p, a modest appreciation from the current share price of 480p.

Jackson is a core part of the editorial team at GoodMoneyGuide.com.

With over 15 years of industry experience as a financial analyst, he brings a wealth of knowledge and expertise to our content and readers.

Previously, Jackson was the director of Stockcube Research as Head of Investors Intelligence. This pivotal role involved providing market timing advice and research to some of the world’s largest institutions and hedge funds.

Jackson brings a huge amount of expertise in areas as diverse as global macroeconomic investment strategy, statistical backtesting, asset allocation, and cross-asset research.

Jackson has a PhD in Finance from Durham University and has authored over 200 guides for GoodMoneyGuide.com.