“If something cannot go on forever,” observed economist Herb Stein, “it will stop.”

Saying a simple thing like that doesn’t mean people will remember it. Occasionally, emotions take over. Caution is abandoned. Dancing only stops when the music stops. Right now, to paraphrase the former Citi CEO Chuck Prince, many are still dancing (wildly).

Of course, investors are dancing given the still-intact bull run. The S&P 500 Index recently broke new record highs as it rallied above the psychological 5,000 level. The magnitude of its 18-month advance surpasses 50 percent. Many stocks have done much better than this. Think Nvidia (NVDA).

What’s interesting about this leg up from 2022 is that it occurred amidst high interest and inflation rates. In 2022, the same factors caused investors to dump stocks in a panic. Now, they seemingly ignore them. It is like these risk factors no longer exist. Even the threat of another rate rise failed to dampen risk sentiment. Last time I looked, Bitcoin was trading above $69,000. That’s how ‘risk on’ the market is.

Given this widespread complacency, it is time to re-assess the market outlook?

Well, the warning signs are there. Jeremy Grantham, the investment guru, observed back in March about the current S&P valuation:

Today is in the top percent on the Shiller P/E of all time, and when you start from this level, you have a very hard time going up materially. You’ve done it once or twice, but you’ve only done it for a while: in the last gasp of 1929; in the last gasp of 1999; and notably and most impressively in Japan, where maybe for two and a half years you kept going. And in each case, they ended incredibly badly. So, the price you paid for bucking that kind of law was a very high price.

More interestingly, he mentioned the general conditions of how a bull market starts:

In general, if you want to make a lot of money, and you want to have a long bull market, you need high unemployment, depressed profit margins, and depressed P/Es……..[Right now] We have totally full employment, totally wonderful profit margins. All the things you would not want to start a bull market from. This is where you start bear markets from. Great bull markets start with exactly the opposite. But it always feels wonderful. Peak profit margins, getting there takes years, and it feels nice.

Indeed. Unemployment rates in us US and UK are at 3.9 and 4.3 percent respectively – near the lower side of their historical bands. So the danger of economic deterioration from here is real.

Profit margins, however, are another story though. For many US companies, their profit margins are on track to meet the market’s lofty expectations despite the high borrowing costs. According to Adam Parker in the Financial Times (June 4, paywall), almost 75 percent of the top S&P 500 companies will meet their gross margin targets this year. Two important factors are driving this trend. One is the increased number of software and biotech companies in the market. These sectors are traditionally high-margin commercial setups. Hence they command higher valuation. The second boost to corporate margin is AI. This new tech is helping to increase productivity across the board. Maybe the stock market will only start to soften when corporate margins begin to compress.

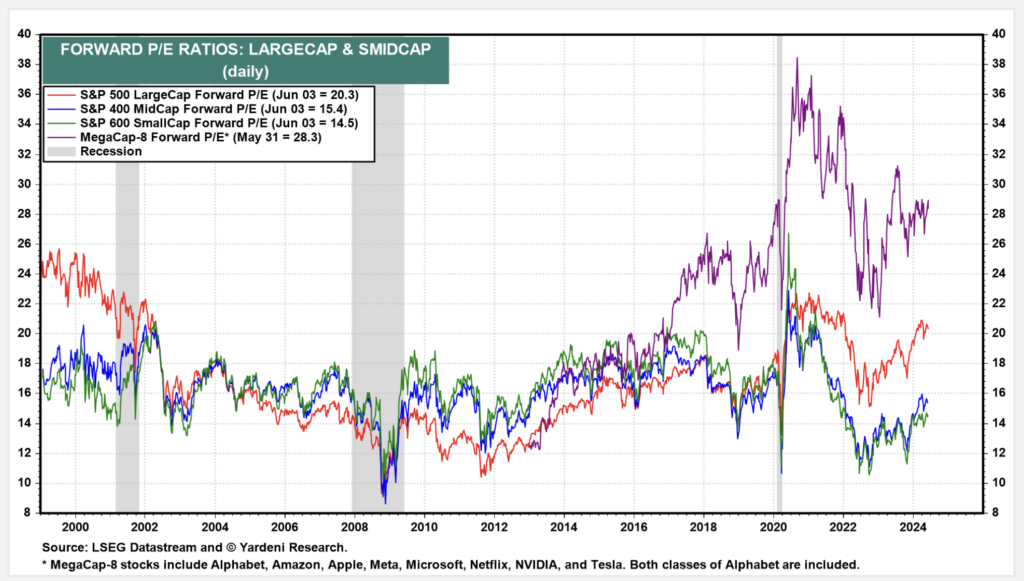

While equity valuation is expensive in the States, does it mean we should start to dump the asset? Not exactly. Valuation is only expensive for the mega caps, as this chart below shows. For the small- and mid-caps, they are trading at half the valuation of mega caps (14 vs 28). Many of the mega caps are software platforms (Google, Microsoft or Meta).

For many small-caps, they are trading near their multi-year lows. A sharp rebound once – in the last swing of a long bull market – is not to be discounted. But this is not a guaranteed rebound. When the mega caps go down, it will drag most stocks down with it. Small caps, with their higher risk profile, may drop further.

Source: Yardeni.com

In the UK, the FTSE 100 Index just broke out of its major resistance at 7,800-8,000 (see below). Valuation is not expensive here either. Normally when a stock index just broke new all-time highs it signals that something is afoot, be it political or economic. As such I not be in a hurry to offload UK stocks as there could be more medium-term upside. Many British stocks are trading at a valuation that appears cheap to foreign companies. M&A may boost investment sentiment here.

In a nutshell, the risk of buying US megacaps is high but there are still pockets of potential opportunities in the stock market.

Featured brokers for investing in US stocks

Jackson is a core part of the editorial team at GoodMoneyGuide.com.

With over 15 years of industry experience as a financial analyst, he brings a wealth of knowledge and expertise to our content and readers.

Previously, Jackson was the director of Stockcube Research as Head of Investors Intelligence. This pivotal role involved providing market timing advice and research to some of the world’s largest institutions and hedge funds.

Jackson brings a huge amount of expertise in areas as diverse as global macroeconomic investment strategy, statistical backtesting, asset allocation, and cross-asset research.

Jackson has a PhD in Finance from Durham University and has authored over 200 guides for GoodMoneyGuide.com.