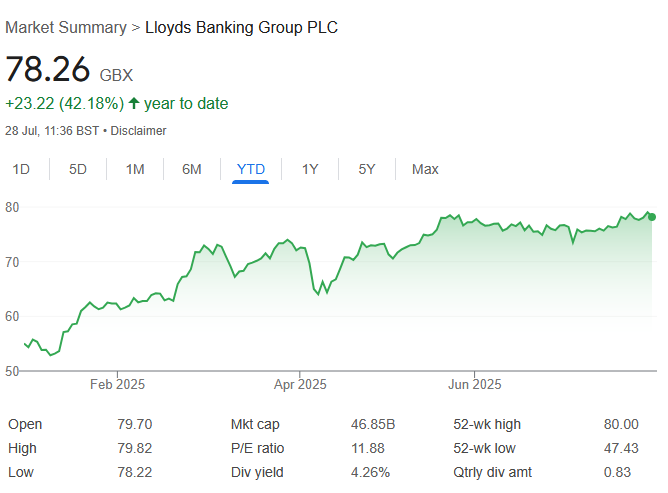

Lloyds (LLOY:LON) shares are in a very strong uptrend at present. This year, they have surged from 55p to 79p – a gain of 44%. Could Lloyds’ share price hit £1 in the near future? Let’s take a look at the set-up for the FTSE 100 bank stock.

Why Lloyds shares are rising in 2025

The backdrop for Lloyds – and other UK bank stocks – looks quite supportive right now. For a start, UK interest rates remain relatively high at 4.25%. This is allowing banks to generate a healthy level of net interest income (NII). For the first half of 2025, Lloyds’ NII was £6.5bn, up 5% year on year.

At the same time, interest rates are coming down. Lower rates should benefit the banks as they’re likely to lead to an increase in borrowing and refinancing activity. Currently, many economists expect another rate cut from the Bank of England in August. There is no guarantee that we will see another rate cut so soon, however.

Another positive is that the credit environment appears to be quite stable. In Lloyds’ H1 results, it told investors that “asset quality remains robust with stable credit performance.” It added that in UK mortgages, reductions in new to arrears and flows to default had been observed over the period. It also noted that credit quality remained stable in commercial banking.

Additionally, stock markets are at high levels. This is a positive for Lloyds’ wealth management and pension operations. Here, fees are generated on assets under management. When stock markets are high like they are now, fees are generally high too.

Is a share price of £1 achievable?

As for whether Lloyds’ share price can hit £1, I think it’s possible. However, I don’t think we’ll see £1 this year. To get to £1, Lloyds’ share price would have to rise 27% from here. And after a 44% gain already this year, I think that kind of gain is unlikely in the second half of 2025.

Looking at the stock’s valuation, Lloyds shares look close to fully valued today. Currently, the forward-looking price-to-earnings (P/E) ratio is about 11. Personally, I’d be surprised if Lloyds was able to command a significantly higher valuation than that. It’s worth noting that the average analyst price target, according to Stockopedia, is 83.6p (about 6% above the current share price).

Looking ahead to 2026, however, the consensus earnings per share (EPS) forecast is 9.5p. That puts the stock on a P/E of just 8.3. There could be some room for multiple expansion there. In other words, we could see the stock rise to near £1 next year.

Risks to the share price

Of course, there are no guarantees that Lloyds shares will hit £1. If the UK economy was to take a turn for the worse, the bank’s share price could go into reverse (the stock is often seen as a proxy for the UK economy).

Another risk that could hurt the share price is liabilities in relation to the motor finance scandal. The Supreme Court is set to deliver a final judgement on alleged mis-selling in the next few weeks.

It’s also worth pointing out that Lloyds shares could potentially see some profit taking as the stock approaches £1 (a major price level). A lot of investors may be tempted to take profits between 95p and £1, putting pressure on the share price.

So, while the stock is moving higher now, investors shouldn’t bank on it hitting £1. That price target is a possibility given the outlook today, but in banking, the outlook can change quickly.

Based in London, Edward is a distinguished investment writer with an extensive client portfolio comprising a diverse array of prominent financial services firms across the globe. With over 15 years of hands-on experience in private wealth management and institutional asset management, both in the UK and Australia, he possesses a profound understanding of the finance industry.

Before establishing himself as a writer, Edward earned a Commerce degree from the prestigious University of Melbourne. Complementing his academic background, he holds the esteemed Investment Management Certificate (IMC) and is a proud holder of the Chartered Financial Analyst (CFA) qualification.

Widely recognised as a sought-after investment expert, Edward’s insightful perspectives and analyses have been featured on sites such as BlackRock, Credit Suisse, WisdomTree, Motley Fool, eToro, and CMC Markets, among others.