Aston Martin Lagonda is one of the most luxurious car companies in the world. However, a world-class brand does not necessarily translate into revenue and profit growth. In this analysis, we explore if Aston Martin is a good company to invest in.

Since AML’s listing back in 2018, the share price has endured a lengthy bear market. Unlike many other cash-rich companies, dilution is a big dampener on the Aston Martin’s share price. In 2018, AML was trading at a (diluted) price of £40. Now? £1.80. AML’s hefty £1.5 billion market cap is no consolation to investors because its size came from an increased share count and not from a high share price.

In recent quarters, arguably, AML stock had performed better. During 2022-2023, for example, AML rallied 250 percent from the £1 psychological support to near £4. But that bull run has reversed as heavy selling dragged the stock once again below £2.

Is Aston Martin a good investment?

The answer depends on your buy-in price. For those investors who stayed with the stock through thick and thin since the pre-pandemic days, the answer is a firm no.

This is due to ballooning corporate losses. The pandemic, in particular, caused the luxury car company to bleed tons of cash. In 2020, it reported £539 million of negative cash flow. Subsequently, new investors were invited (repeatedly) to take stakes in the company. Dilutions, inevitably, put a cap on the Aston Martin share price.

To determine whether AML is a good investment, there are two angles to dissect this problem: Absolute and relative.

Absolute returns

Let’s talk first about the first – absolute investment returns from holding shares in AML.

Since 2018, Aston’s share price appears to head only one way; Down. The fact that AML had two multi-month bull runs was largely inconsequential since, one, those rallies were short in duration and two, prices never returned to the AML IPO level. Many Aston Martin investors are deeply underwater. Even investors who got in late (say last year) now suffer from a steep drawdown in excess of 30 percent.

Relative performance

If AML’s absolute returns appear negative, what about its relative performance? Again, Aston’s shares underperform the market. Here I use the FTSE 100 as the general proxy for the UK stock market.

Since 2018, the FTSE 100 index (ETF ticker ISF) has been fluctuating in a general range. Given the broad recovery in stock price, the UK blue-chip index now trades near the upper side of its range.

In contrast, Aston Martin shares languish near its all-time support levels. The lesson is clear. It would better to stick with The FTSE main market over AML shares.

Moreover, considering that there are many car stocks out there, why should anyone stick with Aston? For sure, Aston supercars are sleek, powerful and head-turning. But a rational mind is needed when you invest your hard-earned cash.

- Expert guide – How to invest in a recession

Compare Aston with Ferrari (ticker: RACE). Since 2015, the legendary Italian sports car company has been listed on the US stock exchange and is now fetching a market cap excess of euro 75 billion. Even though both Ferrari’s and Aston’s cars belong to the premium high-performance category, their share price trend could not be more different.

Look at Ferrari’s long-term chart below. Its trend is clearly positive, long-term bullish and absolutely out-paces AML. Ferrari even hit a new all-time high in early 2024. Plus Ferrari’s are faster.

Why, then, should you stick with a market laggard that still faces an uncertain future when there are much better auto stocks out there? If you insist on owning a car stock, at least pick one that is on a rising trend.

Aston Martin’s long-term prospects

Enough about Aston’s problem. Are there any positive investment points that I can make about Aston Martin?

AML could be a good recovery play if you’re convinced that it has a long-term future. Plenty of smart institutional investors have sunk hundreds of millions into it. In a way, AML is a money pit really.

They wouldn’t have done that if they didn’t envisage a rebound (of some sort, at some point).

Over time, Aston’s car operation appears to be losing less money. In 2023, its losses halved, to a manageable £226 million. In addition, the company is still selling thousands of supercars all over the world (eg, the sleek DB12). The London-listed firm is also pausing its electric car, which may help with its finances. Aston Martin has a strong F1 formula team, too. The Aston Martin F1 racing unit was valued at $1 billion as recently as Nov 2023.

Perhaps the biggest buying point is this: Aston Martin remains a functioning auto-manufacturer after seven bankruptcies in a century! This is impressive. Surely, the brand must be worth something given it was resurrected from the dead so many times.

The only question to discuss is how much that ‘something’ is worth. Some say more than the £1.45 billion that the market is valuing AML right now (equity capitalisation) – given Aston Martin’s annual sales exceeding £1.6 billion. This is the bet that many investors are willing to take.

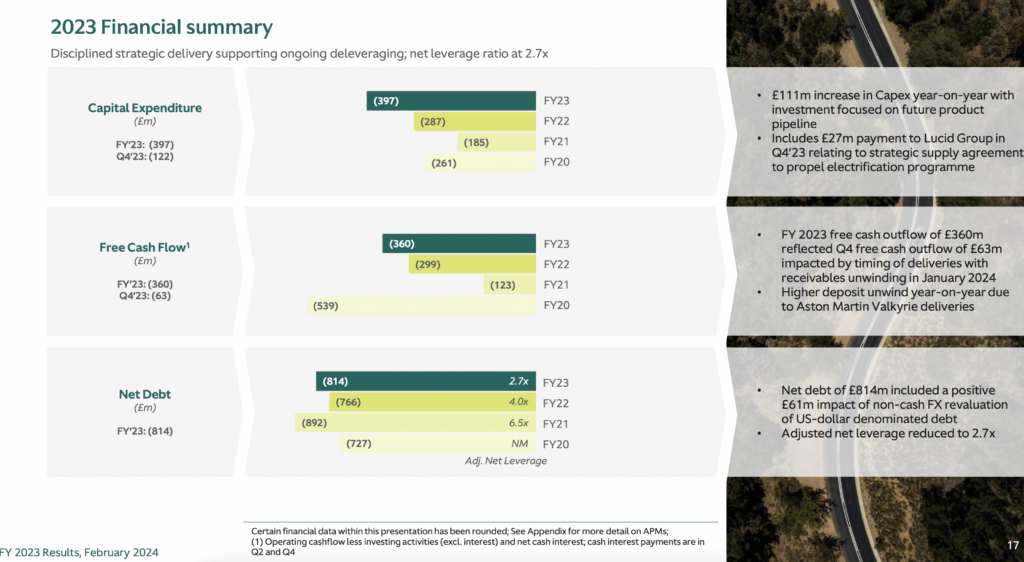

Not to forget, however, is the near £0.9 billion debt load Aston Martin is carrying. Last year, its net debt rose to £814 million on higher capital expenditure and negative cash flow. Whether or not AML is overvalued now is besides the point. The stock is always vulnerable to further dilutive actions because of its negative free cash flow.

Source: Aston Martin plc (2024 Presentation)

Culturally the UK – despite having a large and developed market – appears unsuited to owning or operating a local car brand. I have no idea why. Many UK-based car companies have fallen by the wayside. Perhaps the country is better at selling cars.

Look at Autotrader (AUTO). The online car listing website is worth 2-3x AML’s market capitalisation (£6.7 billion vs £1.5 billion). And unlike Aston Martin, Autotrader is generating good profits (first-half operating profits for 2024 rose to £164 million).

Even car dealers appear to be better investments than AML. For example, in 2023 the Canadian Alpha Auto Group recently bought Lookers (LOOK) in a £460+ million deal. Pendragon’s (PDG) car dealership was acquired by US-based Lithia for £280 million. If given a choice investors should at other auto-related stocks apart from traditional car manufacturers.

If you have some spare cash, perhaps buying a head-turning Aston Martin sports car (DB12 Volante) is better than buying Aston Martin’s shares. At least the car will leave you with a smile.

AML share price regression

In the first half of 2023, AML rebounded strongly following a lengthy bear trend. This oversold rebound, however, lasted less than a year. It promptly ran out of steam by October last year. The break beneath the 320p support completed a medium-term top formation.

Since then, the AML share price has declined substantially, wiping out half the rally in 2022.

What’s next for the Aston Martin share price? Technically AML stock is still in a downtrend (lower low and lower high). More worryingly, the 200p level, which previously acted as support, may have converted into resistance (see below).

Therefore, I would give this downtrend the benefit of the doubt. Until prices started to rebound with large upward dynamics, I would not seek to enter AML on the long side for the time being. The market is just too volatile these days. Tight stops are recommended.

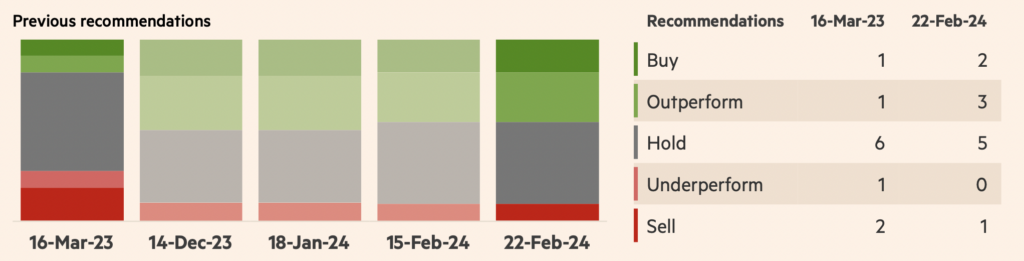

Analysts’ prediction of a company’s share price often depends on the market conditions and in 2022, fear permeated across sectors. Many brokers were deeply skeptical on AML’s ability to weather the difficult consumer environment. Many rated AML ‘Sell’ or ‘Underperform’.

These days, the market is more upbeat about the luxury car company. The balance of opinion is more neutral with a few more bullish recommendations.

Among the 10 analysts following Aston Martin, the median stock price target for AML is 280p.

Source: Financial Times

Jackson is a core part of the editorial team at GoodMoneyGuide.com.

With over 15 years of industry experience as a financial analyst, he brings a wealth of knowledge and expertise to our content and readers.

Previously, Jackson was the director of Stockcube Research as Head of Investors Intelligence. This pivotal role involved providing market timing advice and research to some of the world’s largest institutions and hedge funds.

Jackson brings a huge amount of expertise in areas as diverse as global macroeconomic investment strategy, statistical backtesting, asset allocation, and cross-asset research.

Jackson has a PhD in Finance from Durham University and has authored over 200 guides for GoodMoneyGuide.com.